Fintech

SEC Adopts Amendments to Improve Financial Disclosures about Acquisitions and Dispositions of Businesses

Washington, D.C.–(Newsfile Corp. – May 21, 2020) – The Securities and Exchange Commission today announced that it has voted to adopt amendments to its rules and forms to improve for investors the financial information about acquired or disposed businesses, facilitate more timely access to capital, and reduce the complexity and costs to prepare the disclosure. The amendments will update our rules which have not been comprehensively addressed since their adoption, some over 30 years ago.

“This action, which is designed to enhance the quality of information that investors receive while eliminating unnecessary costs and burdens, will benefit investors, registrants and the market more generally,” said Chairman Jay Clayton. “I want to thank the staff for their outstanding efforts to bring their years of experience to modernizing these rules.”

The amendments to the rules and forms are intended to assist registrants in making more meaningful determinations of whether a subsidiary or an acquired or disposed business is significant, and improve the financial disclosure requirements applicable to acquisitions and dispositions of businesses, including real estate operations and investment companies.

The amendments will be effective on Jan. 1, 2021, but voluntary compliance will be permitted in advance of the effective date.

***

FACT SHEET

Amendments to Financial Disclosures About Acquired and Disposed Businesses

May 21, 2020

Action

The Securities and Exchange Commission today announced that it has adopted amendments to the financial disclosure requirements in Regulation S-X for acquisitions and dispositions of businesses, including real estate operations, in Rules 3-05, 3-14, 8-04, 8-05, 8-06, and Article 11, as well as in other related rules and forms. In conjunction with these changes, the Commission also amended the significance tests in the “significant subsidiary” definition in Rule 1-02(w), Securities Act Rule 405, and Exchange Act Rule 12b-2 to improve their application and to assist registrants in making more meaningful determinations of whether a subsidiary or an acquired or disposed business is significant. In addition, to address the unique attributes of investment companies and business development companies, the Commission adopted new requirements regarding fund acquisitions specific to registered investment companies and business development companies.

Background

When a registrant acquires a significant business, other than a real estate operation, Rule 3-05 of Regulation S-X generally requires a registrant to provide separate audited annual and unaudited interim pre-acquisition financial statements of that business. The number of years of financial information that must be provided depends on the relative significance of the acquisition to the registrant. Similarly, Rule 3-14 of Regulation S-X addresses the unique nature of real estate operations and requires a registrant that has acquired a significant real estate operation to file financial statements with respect to such acquired operation.

Article 11 of Regulation S-X also requires registrants to file unaudited pro forma financial information relating to the acquisition or disposition. Pro forma financial information typically includes a pro forma balance sheet and pro forma income statements based on the historical financial statements of the registrant and the acquired or disposed business, including adjustments to show how the acquisition or disposition might have affected those financial statements.

Rule 3-05 also applies to registrants that are registered investment companies and business development companies. Investment company registrants differ from non-investment company registrants in that they principally invest for returns from capital appreciation and/or investment income, are required to recognize changes in value to their portfolio investments each reporting period, and generally do not consolidate entities they control or use equity method accounting. Due to the nature of registered investment companies and business development companies, under the current rules it is often unclear how to apply these reporting requirements to acquired funds.

Highlights

The final amendments will, among other things:

- update the significance tests in Rule 1-02(w), Securities Act Rule 405, and Exchange Act Rule 12b-2 by:

- revising the investment test to compare the registrant’s investments in and advances to the acquired or disposed business to the registrant’s aggregate worldwide market value if available;

- revising the income test by adding a revenue component;

- expanding the use of pro forma financial information in measuring significance; and

- conforming, to the extent applicable, the significance threshold and tests for disposed businesses to those used for acquired businesses;

- modify and enhance the required disclosure for the aggregate effect of acquisitions for which financial statements are not required or are not yet required by eliminating historical financial statements for insignificant businesses and expanding the pro forma financial information to depict the aggregate effect in all material respects;

- require the financial statements of the acquired business to cover no more than the two most recent fiscal years;

- permit disclosure of financial statements that omit certain expenses for certain acquisitions of a component of an entity;

- permit the use of, or reconciliation to, International Financial Reporting Standards as issued by the International Accounting Standards Board in certain circumstances;

- no longer require separate acquired business financial statements once the business has been included in the registrant’s post-acquisition financial statements for nine months or a complete fiscal year, depending on significance;

- align Rule 3-14 with Rule 3-05 where no unique industry considerations exist;

- clarify the application of Rule 3-14 regarding:

- the determination of significance;

- the need for interim income statements;

- special provisions for blind pool offerings; and

- the scope of the rule’s requirements;

- amend the pro forma financial information requirements to improve the content and relevance of such information; more specifically, the revised pro forma adjustment criteria will provide for:

- “Transaction Accounting Adjustments” reflecting only the application of required accounting to the transaction;

- “Autonomous Entity Adjustments” reflecting the operations and financial position of the registrant as an autonomous entity if the registrant was previously part of another entity; and

- optional “Management’s Adjustments” depicting synergies and dis-synergies of the acquisitions and dispositions for which pro forma effect is being given if, in management’s opinion, such adjustments would enhance an understanding of the pro forma effects of the transaction and certain conditions related to the basis and the form of presentation are met;

- make corresponding changes to the smaller reporting company requirements in Article 8 of Regulation S-X, which will also apply to issuers relying on Regulation A;

- amend the definition of “significant subsidiary” to provide a definition that is specifically tailored for investment companies; and

- add new Rule 6-11 and amend Form N-14 to cover financial reporting for fund acquisitions by investment companies and business development companies.

What’s Next?

The amendments will be effective Jan. 1, 2021. However, voluntary compliance with the final amendments will be permitted in advance of the effective date.

Modern brands stake on influencer marketing, with 76% of users making a purchase after seeing a product on social media.The cryptocurrency industry is no exception to this trend. However, promoting crypto products through influencer marketing can be particularly challenging. Crypto influencers pose a significant risk to a brand’s reputation and ROI due to rampant scams. Approximately 80% of channels provide fake statistics, including followers counts and engagement metrics. Additionally, this niche is characterized by high CPMs, which can increase the risk of financial loss for brands.

In this article Nadia Bubennnikova, Head of agency Famesters, will explore the most important things to look for in crypto channels to find the perfect match for influencer marketing collaborations.

-

Comments

There are several levels related to this point.

LEVEL 1

Analyze approximately 10 of the channel’s latest videos, looking through the comments to ensure they are not purchased from dubious sources. For example, such comments as “Yes sir, great video!”; “Thanks!”; “Love you man!”; “Quality content”, and others most certainly are bot-generated and should be avoided.

Just to compare:

LEVEL 2

Don’t rush to conclude that you’ve discovered the perfect crypto channel just because you’ve come across some logical comments that align with the video’s topic. This may seem controversial, but it’s important to dive deeper. When you encounter a channel with logical comments, ensure that they are unique and not duplicated under the description box. Some creators are smarter than just buying comments from the first link that Google shows you when you search “buy YouTube comments”. They generate topics, provide multiple examples, or upload lists of examples, all produced by AI. You can either manually review the comments or use a script to parse all the YouTube comments into an Excel file. Then, add a formula to highlight any duplicates.

LEVEL 3

It is also a must to check the names of the profiles that leave the comments: most of the bot-generated comments are easy to track: they will all have the usernames made of random symbols and numbers, random first and last name combinations, “Habibi”, etc. No profile pictures on all comments is also a red flag.

LEVEL 4

Another important factor to consider when assessing comment authenticity is the posting date. If all the comments were posted on the same day, it’s likely that the traffic was purchased.

2. Average views number per video

This is indeed one of the key metrics to consider when selecting an influencer for collaboration, regardless of the product type. What specific factors should we focus on?

First & foremost: the views dynamics on the channel. The most desirable type of YouTube channel in terms of views is one that maintains stable viewership across all of its videos. This stability serves as proof of an active and loyal audience genuinely interested in the creator’s content, unlike channels where views vary significantly from one video to another.

Many unauthentic crypto channels not only buy YouTube comments but also invest in increasing video views to create the impression of stability. So, what exactly should we look at in terms of views? Firstly, calculate the average number of views based on the ten latest videos. Then, compare this figure to the views of the most recent videos posted within the past week. If you notice that these new videos have nearly the same number of views as those posted a month or two ago, it’s a clear red flag. Typically, a YouTube channel experiences lower views on new videos, with the number increasing organically each day as the audience engages with the content. If you see a video posted just three days ago already garnering 30k views, matching the total views of older videos, it’s a sign of fraudulent traffic purchased to create the illusion of view stability.

3. Influencer’s channel statistics

The primary statistics of interest are region and demographic split, and sometimes the device types of the viewers.

LEVEL 1

When reviewing the shared statistics, the first step is to request a video screencast instead of a simple screenshot. This is because it takes more time to organically edit a video than a screenshot, making it harder to manipulate the statistics. If the creator refuses, step two (if only screenshots are provided) is to download them and check the file’s properties on your computer. Look for details such as whether it was created with Adobe Photoshop or the color profile, typically Adobe RGB, to determine if the screenshot has been edited.

LEVEL 2

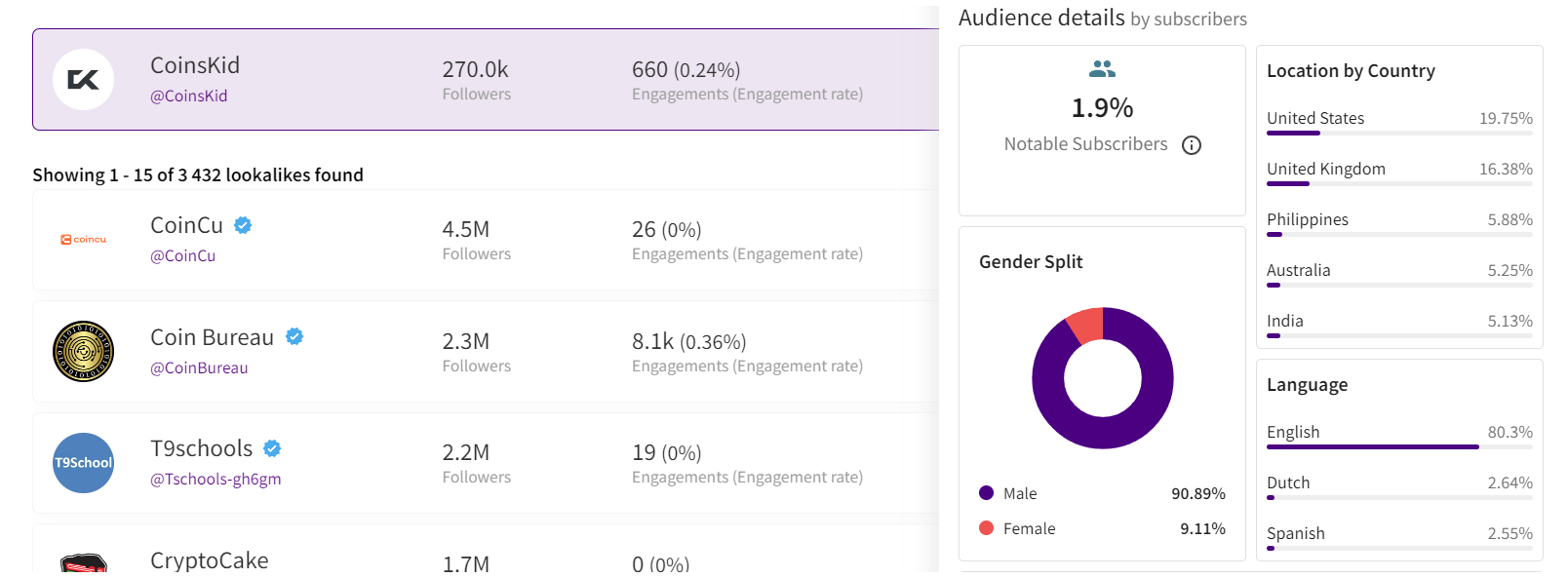

After confirming the authenticity of the stats screenshot, it’s crucial to analyze the data. For instance, if you’re examining a channel conducted in Spanish with all videos filmed in the same language, it would raise concerns to find a significant audience from countries like India or Turkey. This discrepancy, where the audience doesn’t align with regions known for speaking the language, is a red flag.

If we’re considering an English-language crypto channel, it typically suggests an international audience, as English’s global use for quality educational content on niche topics like crypto. However, certain considerations apply. For instance, if an English-speaking channel shows a significant percentage of Polish viewers (15% to 30%) without any mention of the Polish language, it could indicate fake followers and views. However, if the channel’s creator is Polish, occasionally posts videos in Polish alongside English, and receives Polish comments, it’s important not to rush to conclusions.

Example of statistics

Example of statistics

Wrapping up

These are the main factors to consider when selecting an influencer to promote your crypto product. Once you’ve launched the campaign, there are also some markers to show which creators did bring the authentic traffic and which used some tools to create the illusion of an active and engaged audience. While this may seem obvious, it’s still worth mentioning. After the video is posted, allow 5-7 days for it to accumulate a basic number of views, then check performance metrics such as views, clicks, click-through rate (CTR), signups, and conversion rate (CR) from clicks to signups.

If you overlooked some red flags when selecting crypto channels for your launch, you might find the following outcomes: channels with high views numbers and high CTRs, demonstrating the real interest of the audience, yet with remarkably low conversion rates. In the worst-case scenario, you might witness thousands of clicks resulting in zero to just a few signups. While this might suggest technical issues in other industries, in crypto campaigns it indicates that the creator engaged in the campaign not only bought fake views and comments but also link clicks. And this happens more often than you may realize.

Summing up, choosing the right crypto creator to promote your product is indeed a tricky job that requires a lot of resources to be put into the search process.

Author

Nadia Bubennikova, Head of agency at Famesters

The BIS, along with seven leading central banks and a cohort of private financial firms, has embarked on an ambitious venture known as Project Agorá.

Named after the Greek word for “marketplace,” this initiative stands at the forefront of exploring the potential of tokenisation to significantly enhance the operational efficiency of the monetary system worldwide.

Central to this pioneering project are the Bank of France (on behalf of the Eurosystem), the Bank of Japan, the Bank of Korea, the Bank of Mexico, the Swiss National Bank, the Bank of England, and the Federal Reserve Bank of New York. These institutions have joined forces under the banner of Project Agorá, in partnership with an extensive assembly of private financial entities convened by the Institute of International Finance (IIF).

At the heart of Project Agorá is the pursuit of integrating tokenised commercial bank deposits with tokenised wholesale central bank money within a unified, public-private programmable financial platform. By harnessing the advanced capabilities of smart contracts and programmability, the project aspires to unlock new transactional possibilities that were previously infeasible or impractical, thereby fostering novel opportunities that could benefit businesses and consumers alike.

The collaborative effort seeks to address and surmount a variety of structural inefficiencies that currently plague cross-border payments. These challenges include disparate legal, regulatory, and technical standards; varying operating hours and time zones; and the heightened complexity associated with conducting financial integrity checks (such as anti-money laundering and customer verification procedures), which are often redundantly executed across multiple stages of a single transaction due to the involvement of several intermediaries.

As a beacon of experimental and exploratory projects, the BIS Innovation Hub is committed to delivering public goods to the global central banking community through initiatives like Project Agorá. In line with this mission, the BIS will soon issue a call for expressions of interest from private financial institutions eager to contribute to this ground-breaking project. The IIF will facilitate the involvement of private sector participants, extending an invitation to regulated financial institutions representing each of the seven aforementioned currencies to partake in this transformative endeavour.

Source: fintech.globa

The post Central banks and the FinTech sector unite to change global payments space appeared first on HIPTHER Alerts.

TD Bank has inked a multi-year deal with Google Cloud as it looks to streamline the development and deployment of new products and services.

The deal will see the Canadian banking group integrate the vendor’s cloud services into a wider portion of its technology solutions portfolio, a move which TD expects will enable it “to respond quickly to changing customer expectations by rolling out new features, updates, or entirely new financial products at an accelerated pace”.

This marks an expansion of the already established relationship between TD Bank and Google Cloud after the group previously adopted the vendor’s Google Kubernetes Engine (GKE) for TD Securities Automated Trading (TDSAT), the Chicago-based subsidiary of its investment banking unit, TD Securities.

TDSAT uses GKE for process automation and quantitative modelling across fixed income markets, resulting in the development of a “data-driven research platform” capable of processing large research workloads in trading.

Dan Bosman, SVP and CIO of TD Securities, claims the infrastructure has so far supported TDSAT with “compute-intensive quantitative analysis” while expanding the subsidiary’s “trading volumes and portfolio size”.

TD’s new partnership with Google Cloud will see the group attempt to replicate the same level of success across its entire portfolio.

Source: fintechfutures.com

The post TD Bank inks multi-year strategic partnership with Google Cloud appeared first on HIPTHER Alerts.

-

Latest News6 days ago

China remains stabilizing force for global economic growth

-

Latest News5 days ago

Kylian Mbappé and Accor Forge Alliance to Empower Younger Generations

-

Latest News3 days ago

Martello Re announces closing of $1.3 billion capital raise consisting of $935 million in equity and a $360 million upsize of the Company’s credit facility

-

Latest News4 days ago

BioCatch completes best first half in company history, grows ARR by 43% YoY

-

Latest News4 days ago

Market Dojo Celebrates Prestigious Inclusion in Ardent Partners 2024 Strategic Sourcing Technology Advisor

-

Latest News2 days ago

Driving Innovation Forward: CFI Welcomes Seven-Time Formula 1™ World Champion Lewis Hamilton as new Global Brand Ambassador

-

Latest News2 days ago

KEYSTONE BANK HOLDS CUSTOMER FORUM, REITERATES COMMITMENT TO EXCELLENT SERVICE DELIVERY

-

Latest News5 days ago

COP28 President calls on all stakeholders to bring spirit of solidarity that delivered UAE Consensus to drive implementation and sustainable socio-economic development