Fintech

Peter H. Smith and the Concerned Shareholders of Fancamp Continue to Oppose Proposed Highly Dilutive, Self-serving, and Non-arm’s Length Transaction with Scozinc Mining Ltd. and Question the Merits of the Transaction.

- Concerned Shareholders highlight that Fancamp shareholders have suffered too long from conflicted corporate governance and value destroying management.

- Concerned Shareholders demand that the mandate of the board be determined by a long overdue vote of shareholders at an AGM prior to the Transaction with ScoZinc.

- Concerned Shareholders question the merits of the plan of arrangement with ScoZinc.

- Concerned Shareholders demand that Fancamp attain shareholder approval regarding the plan of arrangement with ScoZinc.

- Concerned Shareholders question the mandate of the current board and the dishonest motives behind the delay to the AGM.

- Concerned Shareholders demand that Mark Billings and Ashwath Mehra resign from the board of Fancamp immediately.

- Concerned Shareholders demand that the TSXV intervene to not allow Fancamp to disenfranchise shareholders with such a dilutive transaction without a shareholder vote.

Montreal, Quebec–(Newsfile Corp. – March 1, 2021) – Incumbent director of Fancamp, Peter H. Smith, who, together with joint actors holds in aggregate, directly and indirectly an aggregate of 15,416,097 shares, representing approximately 9.28% of the Company’s issued and outstanding common shares, and a group of concerned shareholders of Fancamp Exploration Ltd. (“Fancamp” or the “Company”) (the “Concerned Shareholders”), are extremely disheartened with the announcement on February 18, 2021 of Fancamp’s highly dilutive, self-serving and non-arm’s length transaction with ScoZinc Mining Ltd. (“ScoZinc”) whereby Fancamp will indirectly acquire all of the issued and outstanding securities of ScoZinc by way of a plan of arrangement (the “Arrangement”) under the Business Corporations Act (British Columbia) (the “Combination” or the “Transaction”) without requesting shareholders of Fancamp to provide shareholder approval for the Transaction.

Several facts were suspiciously omitted from the rightful owners of Fancamp – YOU, the shareholders – which bring to the forefront several questions about the merits of the Transaction and further highlight why a shareholder vote is necessary to approve this Transaction. The Concerned Shareholders have received several calls and emails from shareholders expressing their displeasure with the Transaction and demanding that their voices be heard. Interestingly, the same individuals that are promoting the Transaction are behind the lack of proper disclosure, and poor corporate governance that includes disenfranchising shareholders of the Company by not announcing a date for the annual general meeting (“AGM”) for 2020 and receiving an unjustifiable extension from the BC Registrar of Companies of the time within which it is required to hold its AGM for the year 2020 by six months from December 31, 2020, to June 30, 2021. The Concerned Shareholders reiterate that they want the following: (a) a vote on the composition of the board at an AGM prior to the closing of the Transaction with ScoZinc and (b) their voices to be heard with respect to the ScoZinc Transaction (i.e., attain shareholder approval at an AGM).

Upon further review of the Transaction agreement posted on SEDAR, there were several important facts that were suspiciously not disclosed to Fancamp shareholders in Fancamp’s news release announcing the proposed transaction which would highlight why it is imperative to have Fancamp shareholders vote on the Transaction. Below is a list of omissions and questions that need to be addressed by Fancamp and ScoZinc publicly prior to this Transaction closing. Furthermore, these omissions and questions should force the TSX Venture Exchange (“TSXV”) to inform Fancamp that shareholder approval is required for such a dilutive non-arm’s length transaction. They are as follows:

- A critical fact that was absent from the announcement of the proposed Transaction was that Mr. Smith, as an independent director for the purposes of applicable securities laws relating to matters concerning the rights of minority shareholders in connection with the Transaction, voted against the Transaction.

- Ashwath Mehra and Mark Billings are both Fancamp directors who have a conflict of interest with respect to the Transaction. Rajesh Sharma was recently appointed, not elected to the board, by these two conflicted directors. Therefore, only two elected independent directors voted on the Transaction and one of them (Mr. Smith) voted against the Transaction.

- There is no mention that Ashwath Mehra, in addition to being a director of ScoZinc, is also a large shareholder of ScoZinc and, as a result, stands to significantly benefit personally from the transaction. According to SEDI filings and the latest interim statements for ScoZinc, Mr. Mehra holds 1,538,334 ScoZinc shares, 1,338,334 warrants exercisable at $0.50 and 40,000 options exercisable at $0.52. Upon completion of the Transaction, he is due to receive 9,230,004 Fancamp shares, 8,030,004 warrants exercisable at $0.0833 and 240,000 options exercisable at $0.0867. Based on an $0.11 share price for Fancamp and assuming full dilution less the cost of exercising the warrants and options, Mr. Mehra will gain approximately $1.24 million from the Transaction. Existing shareholders of Fancamp will gain nothing!

- There is no mention of the related nature of the relationships of the ScoZinc board and management and the Fancamp board members and management. Mr. Mark Haywood, Mr. Simon Candrea, Mr. Ashwath Mehra and Mr. Mark Billings all started at ScoZinc within two (2) months of each other (August 2019-October 2019) and will all be on the new Fancamp board and/or management once the Transaction closes. This highlights the related nature of the relationships at play and leaves one to believe that this has been carefully orchestrated. This type of behaviour is unacceptable and from a governance perspective is even more reason to require shareholder approval to legitimize the board’s decision.

- There is no mention that Mark Billings was a director of both companies until he resigned from ScoZinc’s board on December 2, 2020, inexplicably less than one month after being re-elected as a director at ScoZinc’s AGM held on November 3, 2020. Despite this disclosable conflict of interest in the transaction, Billings has refused to recuse himself from voting on the Transaction.

- There is no mention as to the date of Ernst & Young LLP fairness opinion and what valuation metrics used to complete the fairness opinion. If anything, the fairness opinion should be posted to SEDAR so that it may be independently evaluated by Fancamp shareholders.

- The Transaction will result in the issue of approximately 84.5 million shares to bring the Fancamp issued and outstanding share count to approximately 250.5 million representing dilution to existing Fancamp shareholders of 33.7%. On a fully diluted basis existing Fancamp shareholders will be giving 44.3% of THEIR company to ScoZinc shareholders and the share structure will increase 317.0 million shares!

- According to the latest available SEDAR filings, as at September 30, 2020 ScoZinc reported working capital of only $68,574 (ScoZinc Management and Discussion and Analysis dated November 5, 2020) and is essentially insolvent compared to Fancamp with reported working capital of $17,042,721 as at October 31, 2020 (Fancamp Management and Discussion and Analysis dated December 30, 2020).

- Despite ScoZinc management glowingly referring to the “Scotia Mine’s robust Pre-Feasibility Study in July 2020” in a press release dated February 26, 2021, they have failed to secure any binding equity, debt or offtake agreements to finance the project, and without high jacking Fancamp’s treasury it is unlikely that any financing would be forthcoming for this project on its own merits. Furthermore, ScoZinc’s management failed to mention in the press release whether they have received an interim order which was stipulated in the arrangement agreement to be obtained by February 26, 2021, further highlighting that ScoZinc, like Fancamp’s incumbent management, has poor disclosure and governance practices.

- Why has Fancamp’s 2020 AGM been delayed when, if held, would provide shareholders with an opportunity to voice their opinion as to whether this proposed transaction should proceed, particularly when Fancamp previously represented it would hold its AGM in the first quarter of 2021?

The Concerned Shareholders urge the TSXV to immediately notify Fancamp that shareholder approval must be attained before any plan of arrangement can be consummated. This transaction is rife with conflicts that have not been properly disclosed to shareholders of Fancamp. The behaviour of Mr. Billings, Mr. Mehra and Mr. Sharma highlight the lack of respect they have for Fancamp shareholders and underscores that these individuals feel that they can do whatever they want. It is clear they have forgotten their accountability and apparently feel they can manipulate various rules and policies that are in place to protect shareholders to their advantage with impunity. This must stop, and it must stop now.

The proposed Combination is yet another misguided move by an entrenched Fancamp board and management team that claim this Transaction is for the betterment of the Company and its shareholders but in reality is being done to further their own self-interests in complicity with ScoZinc insiders who will increase their interest in Fancamp from less than 1% to 18% fully diluted. Moreover, ScoZinc directors Mark Haywood and Chris Hopkins will be nominated to, and with Mr. Billings, Mr. Mehra and Mr. Sharma, will control the post-Transaction board of Fancamp. In addition, Mr. Haywood, who is ScoZinc’s current CEO, and Mr. Simion Candrea vice-president, investor relations of ScoZinc, will have their contracts assumed by Fancamp resulting in ScoZinc’s current board and management members comprising a majority of Fancamp’s board and management on closing of the Combination. It is clear that these decisions further entrench the conflicted incumbent board members of Fancamp and stifle the voices of any truly independent director of Fancamp which runs counter to any desire to run an organization with good corporate governance.

Additionally, the Concerned Shareholders find it incomprehensible that shareholder approval is not required in the face of known public agitations by the Concerned Shareholders expressing the intent to remove various members of the board of Fancamp. For this transaction to be announced prior to the long overdue 2020 AGM is outrageous and a slap in the face for all Fancamp shareholders.

The Concerned Shareholders would like to thank the number of shareholders that have contacted them or Gryphon Advisors Inc. to express their support and sharing stories of inappropriate behaviour exhibited by Mr. Mehra. The Concerned Shareholders look forward to engaging with each Fancamp shareholder when legally appropriate.

For more information regarding the Concerned Shareholders’ position please contact:

Gryphon Advisors Inc.

Tel: 1-833-461-3651

Email: [email protected]

Information in Support of Public Broadcast Solicitation

The information contained in this press release does not and is not meant to constitute a solicitation of a proxy within the meaning of applicable securities laws. Although the Concerned Shareholders have approached several nominees for election to the Company’s board of directors at the company’s next general meeting of shareholders, there is currently no record or meeting date set and shareholders are not being asked at this time to execute a proxy in favour of any matter. In connection with the meeting, the Concerned Shareholders may file a dissident information circular in due course in compliance with applicable securities laws.

The information contained herein, and any solicitation made by the Concerned Shareholders in advance of any general meeting of shareholders, or will be, as applicable, made by the Concerned Shareholders and not by or on behalf of the management of Fancamp. All costs incurred for any solicitation will be borne by the Concerned Shareholders, provided that, subject to applicable law, the Concerned Shareholders may seek reimbursement from Fancamp of the Concerned Shareholders’ out-of-pocket expenses, including proxy solicitation expenses and legal fees, incurred in connection with a successful reconstitution of the Company’s board of directors. The Concerned Shareholders are not soliciting proxies in connection with a general meeting of shareholders of the Company at this time.

The Concerned Shareholders may engage the services of one or more agents and authorize other persons to assist in soliciting proxies on behalf of the Concerned Shareholders. Any proxies solicited by or on behalf of the Concerned Shareholders, including by any other agent retained by the Concerned Shareholders, may be solicited pursuant to a dissident information circular or by way of public broadcast, including through press releases, speeches, or publications and by any other manner permitted under Canadian corporate and securities laws. Any such proxies may be revoked by instrument in writing executed by a shareholder or by his or her attorney authorized in writing or, if the shareholder is a body corporate, by an officer or attorney thereof duly authorized or by any other manner permitted by law.

The registered address of Fancamp is located at 3200 – 650 West Georgia Street, Vancouver, BC, V6B 4P7. The mailing and head office address of Fancamp is 7290 Gray Avenue, Burnaby, British Columbia V5J 3Z2. A copy of this press release may be obtained on Fancamp’s SEDAR profile at www.sedar.com.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/75698

Modern brands stake on influencer marketing, with 76% of users making a purchase after seeing a product on social media.The cryptocurrency industry is no exception to this trend. However, promoting crypto products through influencer marketing can be particularly challenging. Crypto influencers pose a significant risk to a brand’s reputation and ROI due to rampant scams. Approximately 80% of channels provide fake statistics, including followers counts and engagement metrics. Additionally, this niche is characterized by high CPMs, which can increase the risk of financial loss for brands.

In this article Nadia Bubennnikova, Head of agency Famesters, will explore the most important things to look for in crypto channels to find the perfect match for influencer marketing collaborations.

-

Comments

There are several levels related to this point.

LEVEL 1

Analyze approximately 10 of the channel’s latest videos, looking through the comments to ensure they are not purchased from dubious sources. For example, such comments as “Yes sir, great video!”; “Thanks!”; “Love you man!”; “Quality content”, and others most certainly are bot-generated and should be avoided.

Just to compare:

LEVEL 2

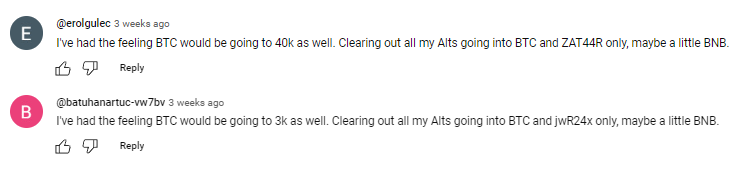

Don’t rush to conclude that you’ve discovered the perfect crypto channel just because you’ve come across some logical comments that align with the video’s topic. This may seem controversial, but it’s important to dive deeper. When you encounter a channel with logical comments, ensure that they are unique and not duplicated under the description box. Some creators are smarter than just buying comments from the first link that Google shows you when you search “buy YouTube comments”. They generate topics, provide multiple examples, or upload lists of examples, all produced by AI. You can either manually review the comments or use a script to parse all the YouTube comments into an Excel file. Then, add a formula to highlight any duplicates.

LEVEL 3

It is also a must to check the names of the profiles that leave the comments: most of the bot-generated comments are easy to track: they will all have the usernames made of random symbols and numbers, random first and last name combinations, “Habibi”, etc. No profile pictures on all comments is also a red flag.

LEVEL 4

Another important factor to consider when assessing comment authenticity is the posting date. If all the comments were posted on the same day, it’s likely that the traffic was purchased.

2. Average views number per video

This is indeed one of the key metrics to consider when selecting an influencer for collaboration, regardless of the product type. What specific factors should we focus on?

First & foremost: the views dynamics on the channel. The most desirable type of YouTube channel in terms of views is one that maintains stable viewership across all of its videos. This stability serves as proof of an active and loyal audience genuinely interested in the creator’s content, unlike channels where views vary significantly from one video to another.

Many unauthentic crypto channels not only buy YouTube comments but also invest in increasing video views to create the impression of stability. So, what exactly should we look at in terms of views? Firstly, calculate the average number of views based on the ten latest videos. Then, compare this figure to the views of the most recent videos posted within the past week. If you notice that these new videos have nearly the same number of views as those posted a month or two ago, it’s a clear red flag. Typically, a YouTube channel experiences lower views on new videos, with the number increasing organically each day as the audience engages with the content. If you see a video posted just three days ago already garnering 30k views, matching the total views of older videos, it’s a sign of fraudulent traffic purchased to create the illusion of view stability.

3. Influencer’s channel statistics

The primary statistics of interest are region and demographic split, and sometimes the device types of the viewers.

LEVEL 1

When reviewing the shared statistics, the first step is to request a video screencast instead of a simple screenshot. This is because it takes more time to organically edit a video than a screenshot, making it harder to manipulate the statistics. If the creator refuses, step two (if only screenshots are provided) is to download them and check the file’s properties on your computer. Look for details such as whether it was created with Adobe Photoshop or the color profile, typically Adobe RGB, to determine if the screenshot has been edited.

LEVEL 2

After confirming the authenticity of the stats screenshot, it’s crucial to analyze the data. For instance, if you’re examining a channel conducted in Spanish with all videos filmed in the same language, it would raise concerns to find a significant audience from countries like India or Turkey. This discrepancy, where the audience doesn’t align with regions known for speaking the language, is a red flag.

If we’re considering an English-language crypto channel, it typically suggests an international audience, as English’s global use for quality educational content on niche topics like crypto. However, certain considerations apply. For instance, if an English-speaking channel shows a significant percentage of Polish viewers (15% to 30%) without any mention of the Polish language, it could indicate fake followers and views. However, if the channel’s creator is Polish, occasionally posts videos in Polish alongside English, and receives Polish comments, it’s important not to rush to conclusions.

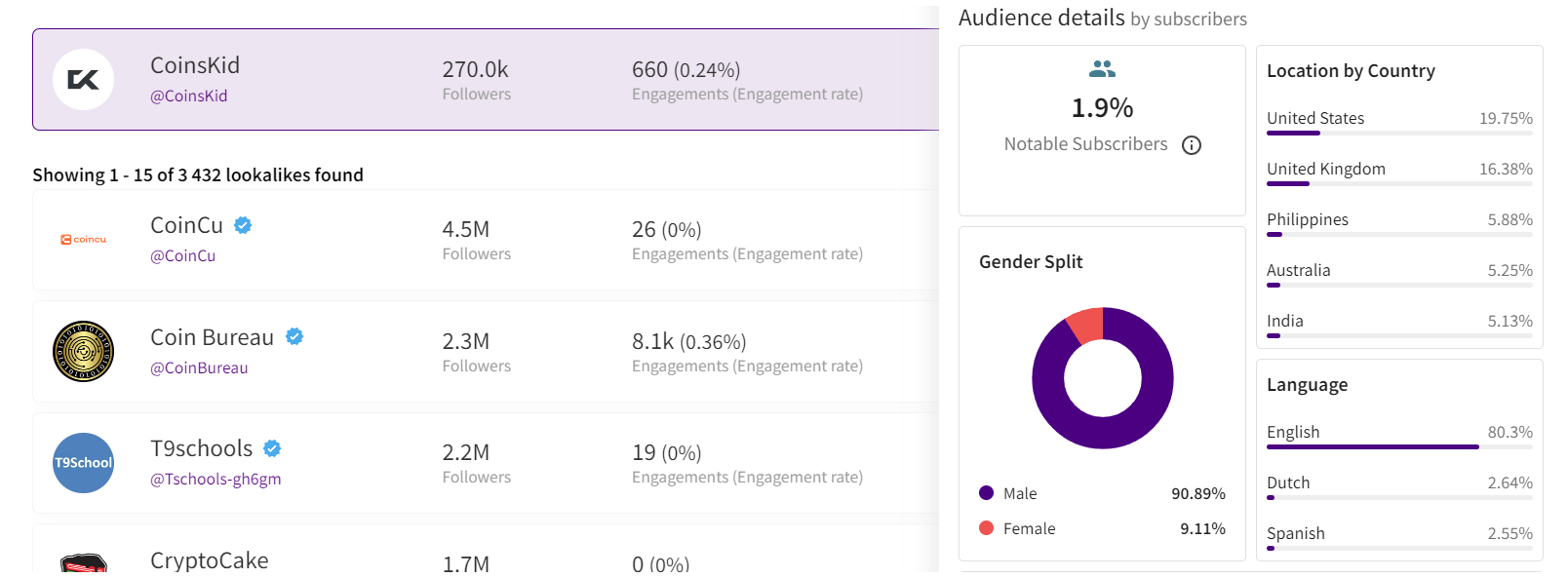

Example of statistics

Example of statistics

Wrapping up

These are the main factors to consider when selecting an influencer to promote your crypto product. Once you’ve launched the campaign, there are also some markers to show which creators did bring the authentic traffic and which used some tools to create the illusion of an active and engaged audience. While this may seem obvious, it’s still worth mentioning. After the video is posted, allow 5-7 days for it to accumulate a basic number of views, then check performance metrics such as views, clicks, click-through rate (CTR), signups, and conversion rate (CR) from clicks to signups.

If you overlooked some red flags when selecting crypto channels for your launch, you might find the following outcomes: channels with high views numbers and high CTRs, demonstrating the real interest of the audience, yet with remarkably low conversion rates. In the worst-case scenario, you might witness thousands of clicks resulting in zero to just a few signups. While this might suggest technical issues in other industries, in crypto campaigns it indicates that the creator engaged in the campaign not only bought fake views and comments but also link clicks. And this happens more often than you may realize.

Summing up, choosing the right crypto creator to promote your product is indeed a tricky job that requires a lot of resources to be put into the search process.

Author

Nadia Bubennikova, Head of agency at Famesters

The BIS, along with seven leading central banks and a cohort of private financial firms, has embarked on an ambitious venture known as Project Agorá.

Named after the Greek word for “marketplace,” this initiative stands at the forefront of exploring the potential of tokenisation to significantly enhance the operational efficiency of the monetary system worldwide.

Central to this pioneering project are the Bank of France (on behalf of the Eurosystem), the Bank of Japan, the Bank of Korea, the Bank of Mexico, the Swiss National Bank, the Bank of England, and the Federal Reserve Bank of New York. These institutions have joined forces under the banner of Project Agorá, in partnership with an extensive assembly of private financial entities convened by the Institute of International Finance (IIF).

At the heart of Project Agorá is the pursuit of integrating tokenised commercial bank deposits with tokenised wholesale central bank money within a unified, public-private programmable financial platform. By harnessing the advanced capabilities of smart contracts and programmability, the project aspires to unlock new transactional possibilities that were previously infeasible or impractical, thereby fostering novel opportunities that could benefit businesses and consumers alike.

The collaborative effort seeks to address and surmount a variety of structural inefficiencies that currently plague cross-border payments. These challenges include disparate legal, regulatory, and technical standards; varying operating hours and time zones; and the heightened complexity associated with conducting financial integrity checks (such as anti-money laundering and customer verification procedures), which are often redundantly executed across multiple stages of a single transaction due to the involvement of several intermediaries.

As a beacon of experimental and exploratory projects, the BIS Innovation Hub is committed to delivering public goods to the global central banking community through initiatives like Project Agorá. In line with this mission, the BIS will soon issue a call for expressions of interest from private financial institutions eager to contribute to this ground-breaking project. The IIF will facilitate the involvement of private sector participants, extending an invitation to regulated financial institutions representing each of the seven aforementioned currencies to partake in this transformative endeavour.

Source: fintech.globa

The post Central banks and the FinTech sector unite to change global payments space appeared first on HIPTHER Alerts.

TD Bank has inked a multi-year deal with Google Cloud as it looks to streamline the development and deployment of new products and services.

The deal will see the Canadian banking group integrate the vendor’s cloud services into a wider portion of its technology solutions portfolio, a move which TD expects will enable it “to respond quickly to changing customer expectations by rolling out new features, updates, or entirely new financial products at an accelerated pace”.

This marks an expansion of the already established relationship between TD Bank and Google Cloud after the group previously adopted the vendor’s Google Kubernetes Engine (GKE) for TD Securities Automated Trading (TDSAT), the Chicago-based subsidiary of its investment banking unit, TD Securities.

TDSAT uses GKE for process automation and quantitative modelling across fixed income markets, resulting in the development of a “data-driven research platform” capable of processing large research workloads in trading.

Dan Bosman, SVP and CIO of TD Securities, claims the infrastructure has so far supported TDSAT with “compute-intensive quantitative analysis” while expanding the subsidiary’s “trading volumes and portfolio size”.

TD’s new partnership with Google Cloud will see the group attempt to replicate the same level of success across its entire portfolio.

Source: fintechfutures.com

The post TD Bank inks multi-year strategic partnership with Google Cloud appeared first on HIPTHER Alerts.

-

Fintech4 days ago

Fintech4 days agoHow to identify authenticity in crypto influencer channels

-

Latest News7 days ago

BMO Announces Election of Board of Directors

-

Latest News4 days ago

HSBC-backed fintech Monese is considering splitting its operations as it grapples with increasing losses.

-

Latest News3 days ago

EverBank has announced a groundbreaking partnership with Finzly, poised to revolutionize payment processing.

-

Latest News3 days ago

FinTech leaders express caution regarding the promises made in #Budget2024 concerning open banking, stating that the “devil is in the details.”

-

Latest News3 days ago

Gotion High-tech’s operating profit up 391% in 2023, nearly RMB 2.8 billion invested in R&D for the year

-

Latest News3 days ago

Aurionpro Solutions acquires Arya.ai, to power next generation Enterprise AI platforms for Financial Institutions

-

Latest News4 days ago

Wells Fargo, a leading financial institution, is set to revolutionize its trade finance operations by incorporating artificial intelligence (AI) technology through its collaboration with TradeSun.