Fintech

1287390 B.C. Ltd. Announces Proposed Business Combination Transaction and Concurrent Financing

Toronto, Ontario–(Newsfile Corp. – March 3, 2022) – 1287390 B.C. Ltd. (“390”) is pleased to announce it has entered into an amalgamation agreement dated March 3, 2022] (the “Definitive Agreement“) with NiCAN Limited (“NiCAN” or the “Company“), pursuant to which the Company will amalgamate with 390 and continue as one corporation (the “Transaction“), being the “Resulting Issuer“. As a result of the Transaction, the securityholders of NiCAN and 390 will become securityholders of the Resulting Issuer. Upon completion of the Transaction, the Resulting Issuer (to be named “NiCAN Limited”) will carry on the business of NiCAN, as described herein.

390 anticipates that the Transaction will enable the Resulting Issuer to meet the initial listing requirements of the TSX Venture Exchange (“TSXV“) for a “Tier 2 Mining Issuer” (as such term is defined in the policies of the TSXV).

The Properties

NiCAN was incorporated in April of 2021, focusing on Nickel Sulphide exploration opportunities and projects on known nickel belts in stable jurisdictions. With that objective, NiCAN identified two highly prospective opportunities in Manitoba, the Wine property (the “Wine Property“) in the Flin Flon-Snow Lake area and the Pipy project (the “Pipy Project“) in the Thompson area, both proximal to areas of known nickel mineralization. The Wine Property will be the material property of the Resulting Issuer and the Qualifying Property (as defined in the policies of the TSXV).

With strong support from stakeholders and the Board of Directors, NiCAN rapidly progressed the projects over the last year. Completing extensive historical data compilation, correction, and evaluation, developing a significantly improved database from which to drive new geologic models and understanding, and drill targets.

The Wine Property

The Wine Property is located within a favourable portion of the highly prospective Flin Flon-Snow Lake Greenstone Belt of Manitoba. The Wine Property was acquired based on the Wine Copper-Nickel Occurrence and given the geology of the Wine Property is favourable for magmatic nickel deposits, characterized by a geological environment categorized by mafic to ultramafic rocks intruding supracrustal rocks.

Previous exploration on the Wine Property area has largely consisted of drill testing of geophysical anomalies. Initial drilling was very much focused on a massive sulphide copper-zinc deposit model and the recognition of the magmatic copper and nickel potential of the Wine Property was not realized until a significant number of drill holes were completed on the property. Because of the early massive sulphide exploration focus, pyrrhotite-rich drill intercepts were not historically assayed for nickel.

The origin of the Wine Copper-Nickel occurrence is interpreted as a mafic-ultramafic-hosted sulphide deposit, resulting from the intrusion of ultramafic to mafic magma into favourable supracrustal rocks containing a source of sulphur. The presence of gabbroic intrusive rocks in the footwall of the Wine Copper-Nickel occurrence and the abundance of juvenile arc volcanic rocks represents a favourable geological environment for the development of magmatic-hosted sulphide deposits.

The inclusion of sulphide-rich country rocks within ultramafic-mafic-hosts is acknowledged to be a critical feature of sulphide nickel deposits worldwide. The general theory of magmatic-hosted sulphide-nickel mineralization involves the assimilation of sulphide-bearing country rocks, which due to elemental characteristics results in nickel, copper, cobalt and other chalcophile elements preferentially concentrating in the sulphide phase, which due to an inherent immiscibility with the silicate-rich ultramafic magma and greater density, sinks to the bottom of the magma chamber forming the nickel-sulphide deposit.

The airborne Total Magnetic image of the Wine Property indicates that the large Little Swan Lake Pluton located to the north of The Wine Copper-Nickel occurrence has a distinct magnetic signature and its emplacement has caused significant folding to the rocks located to the southeast. It is interpreted that significantly more folding, and deformation occurs than is displayed on the available geology maps. This is especially apparent in the Wine Occurrence area and to the northwest.

It is interpreted that the high degree of deformation and high metamorphic grade that characterizes the area has likely resulted in the migration of nickel sulphide mineralization into low strain domains, such as fold hinges and fault zones caused by the intrusion of the Little Swan Lake Pluton thus removing the copper-nickel mineralization from its original host.

NiCAN commenced its first drill program on the Wine Property, in the Flin Flon-Snow Lake area, in January 2022. This drilling campaign will consist of up to 15 diamond drill holes, or up to approximately 1,500m, following up on historical drilling, surveys, and data compilation, testing our reinterpretation of the geologic model at the Wine Occurrence, as well as testing additional highly prospective targets in the more immediate area. Historical drilling on the Wine Occurrence returned significant results including 20.4m of 1.3% nickel and 2.27% copper.

The Pipy Project

The Pipy Project is located 15 kilometres north of the world class Thompson nickel deposit. The claims cover the same geological horizon within Pipe Formation that hosts the Thompson nickel mineralization, and the horizon can be traced for over 14 kilometres wrapped around a folded structure at the Pipy Project.

NiCAN has undertaken extensive data compilation, correction and evaluation at the Pipy Project. The Pipy Project was drilled in the 1960s by INCO, however without the benefit of the structural data available today utilizing newer ground penetrating technology. NiCAN completed an airborne High-definition UAV Magnetometer survey and is utilizing this new structural information in conjunction with the historical drill logs to design an exploration program. NiCAN expects to initiate the permitting phase of this project in the coming months.

A total of 74 historic drill holes are located within or adjacent to the claims comprising the Pipy Project between 1957 to 1971. There is no record of any recent drilling. Historical drilling logs do not include any assay information or detailed descriptions; however, the summary logs were released for most of the drill holes. Nine of the logs drilled in 1968 contain more detail and note sulphide mineralization and mention nickel sulphides. The nickel sulphides can only be produced by a nickel mineralizing system with the same mechanisms that created the Thompson deposit. This highlights the prospective nature of the Pipy Project and these historical drilling logs will be used by NiCAN to direct future geophysical surveys and drilling.

Much of the prospective 14-kilometre-long horizon remains untested. Only 10 holes were drilled below 200-300 metres depth. NiCAN plans to employ modern geophysical surface technologies that can detect sulphide bodies down to a kilometre in depth.

In the era prior to 1971, downhole EM technology was not available to test for massive sulphide bodies adjacent to a drill hole. Any future drilling by NiCAN will employ downhole 3D EM technology that can look up 200 metres adjacent to a drill hole significantly increasing the probability of success and cost effectiveness of each metre drilled.

To further refine future deep geophysical and drilling programs NiCAN has completed a high-resolution magnetic survey over the Pipy Project. Processing is underway to create 3D images of the subsurface and will aid in selecting high priority areas.

Definitive Agreement

The Definitive Agreement between NiCAN and 390 provides for, among other things, a long-form amalgamation under the Business Corporations Act (Ontario) (the “Amalgamation“), pursuant to which: (i) 390 will continue out of the provincial jurisdiction of British Columbia and into the provincial jurisdiction of Ontario (the “Continuance“); (ii) 390 will complete a consolidation of its issued and outstanding common shares on the basis of a ratio to be determined immediately prior to the closing of the Transaction, so that the existing holders of the 390 Shares (as defined below) shall hold, in the aggregate, such number of Resulting Issuer Shares (as defined below) that when multiplied by the NiCAN Share Value (as defined below) equals $1,300,000 (the “Consolidation“), such basis resulting in the deemed value of the post-Consolidation common shares of 390 (each, a “390 Share“) being equal of the NiCAN Share Value; (iii) NiCAN and 390 will effect the Amalgamation at which time they will cease to exist as separate legal entities and continue as one corporation, the Resulting Issuer; (iv) all of the outstanding common shares of NiCAN (each, a “NiCAN Share“) will be cancelled and, in consideration therefor, the holders thereof will receive common shares of the Resulting Issuer (each, a “Resulting Issuer Share“) on the basis of one NiCAN Share for one Resulting Issuer Share; (v) all of the outstanding 390 Shares will be cancelled and, in consideration therefor, the holders thereof will receive Resulting Issuer Shares on the basis of one 390 Share for one Resulting Issuer Share; and (vi) the Resulting Issuer will be named “NiCAN Limited”, or such other name as determined by NiCAN.

Completion of the Transaction will be subject to certain conditions, including among others: (i) the requirement for 390 to obtain approval of all of the shareholders of 390 with respect to the Transaction; (ii) the requirement for NiCAN to obtain approval of all of the shareholders of NiCAN with respect to the Transaction; (iii) the completion of the Offering (as defined below); (iv) the completion of the Consolidation by 390; (v) the approval by the shareholders of 390 of the Continuance and its subsequent completion; (vi) obtaining the approval of the TSXV with respect to the listing of the Resulting Issuer Shares; (vii) the TSXV shall have granted an exemption or waiver from the sponsorship requirement or a sponsor shall have filed an acceptable report with the TSXV; and (viii) 390 shall not be in default of the requirements of any securities commission and no order shall have been issued that would prevent the Transaction or trading of any securities of 390.

For the purposes of the Transaction, the deemed value of each NiCAN Share will be the weighted average offering price of the Subscription Receipts (as defined below) pursuant to the Offering (the “NiCAN Share Value“).

Concurrent Offering

In connection with the Transaction, NiCAN intends to complete a non-brokered private placement of a minimum of 13,000,000 Subscription Receipts (as defined below), in any combination of: (i) non-flow-through subscription receipts (the “HD Subscription Receipts“) at a price of $0.40 per HD Subscription Receipt, and (ii) flow-through subscription receipts (the “FT Subscription Receipts” and together with the HD Subscription Receipts, the “Subscription Receipts“) at a price of $0.45 per FT Subscription Receipt, for aggregate gross proceeds of a minimum of $5,200,000 (collectively, the “Offering“). It is expected that the Company will pay certain eligible persons (each, a “Finder“) a finder’s fee equal to 6.0% of the aggregate gross proceeds of the subscribers participating in the Offering introduced by such Finders (“Finder’s Fee“), payable on the closing date of the Offering. In addition, the Company will issue to such Finders, finder’s warrants (the “Finder’s Warrants“) exercisable to acquire that number of NiCAN Shares as is equal to 6.0% of the aggregate number of Subscription Receipts issued pursuant to the Offering to the subscribers introduced by each such Finder. Each Finder’s Warrant shall be exercisable to acquire one NiCAN Share at a price of $0.40 for a period of 12 months following the closing of the Offering.

The gross proceeds derived from the sale of the Subscription Receipts, less 50% of the Finder’s Fees payable in connection with the Offering, will be held in escrow on behalf of the subscribers of the Subscription Receipts by an escrow agent to be appointed by the Company, pursuant to the terms of a subscription receipt agreement (the “Subscription Receipt Agreement“) to be entered into on or about the closing date of the Offering.

It is expected that each HD Subscription Receipt will be, in accordance with the Subscription Receipt Agreement, automatically converted, without payment of any additional consideration and without any further action on the part of the holder thereof, for one NiCAN Share (each, a “Common Share“) upon the satisfaction of certain conditions related to the Transaction (the “Escrow Release Conditions“). It is expected that each FT Subscription Receipt will be, in accordance with the Subscription Receipt Agreement, automatically converted, without payment of any additional consideration and without any further action on the part of the holder thereof, for one NiCAN Share, issued on a “flow-through basis” (each, a “FT Share“) upon the satisfaction of the Escrow Release Conditions. The FT Shares will qualify as “flow-through shares” within the meaning of the Income Tax Act (Canada). Pursuant to the terms of the Definitive Agreement, the Common Shares and FT Shares will be exchanged for Resulting Issuer Shares on the basis of one Resulting Issuer Share for each Common Share and FT Share so held, respectively.

The net proceeds of the Offering derived from the HD Subscription Receipts will be used by the Company to fund exploration, as well as for general corporate purposes following completion of the Transaction. The aggregate gross proceeds raised from the sale of the FT Subscription Receipts (the “Commitment Amount“) will be used before December 31, 2023 for general exploration expenditures, which will constitute eligible Canadian exploration expenses (within the meaning of subsection 66 (15) of the Income Tax Act (Canada), that will qualify as “flow through mining expenditures” within the meaning of the Tax Act (the “Qualifying Expenditures“). The Company shall renounce the Qualifying Expenditures so incurred to the subscribers of the FT Shares, such that the aggregate Commitment Amount shall be deductible against each such subscriber’s income for the calendar year ended December 31, 2022.

The securities to be offered in the Offering have not been, and will not be, registered under the U.S. Securities Act of 1933, as amended (the “U.S. Securities Act“) or any U.S. state securities laws, and may not be offered or sold in the United States or to, or for the account or benefit of, United States persons absent registration or any applicable exemption from the registration requirements of the U.S. Securities Act and applicable U.S. state securities laws. This news release shall not constitute an offer to sell or the solicitation of an offer to buy securities in the United States, nor shall there be any sale of these securities in any jurisdiction in which such offer, solicitation or sale would be unlawful.

Further details of the Offering will be announced by 390 in a subsequent news release.

Selected Financial Information

The following table sets out selected financial information with respect to NiCAN as at the dates noted. The selected financial information is derived from NiCAN’s financial statements for the periods described and denominated in Canadian dollars.

| As at December 31, 2021 (unaudited) |

|

| Total assets | $ 2,332,837 |

| Total liabilities | 875,712 |

| Shareholders’ equity | 1,457,125 |

| Period from incorporation on April 6, 2021 to December 31, 2021 (unaudited) |

|

| Revenues | 1,343 |

| Net profit (loss) | (1,275,202) |

Further financial information will be included in the listing application to be prepared in connection with the Transaction.

Stock Exchange Matters

As at the date hereof, neither the common shares of 390 nor the NiCAN Shares are listed on any stock exchange in Canada, or elsewhere. 390 is a “reporting issuer” (within the meaning of applicable securities legislation) in the Provinces of British Columbia and Alberta.

A condition to completion of the Transaction is the conditional approval for the listing of the Resulting Issuer Shares on the TSXV as a “Tier 2 Mining Issuer” (within the meaning of the policies of the TSXV). A listing application which will include further details of the Transaction, the Wine Property and the Offering, will be filed on 390’s issuer profile on SEDAR at www.sedar.com, upon TSXV conditional approval of the listing. There can be no assurance that the TSXV will grant such conditional approval or that the Transaction or the Offering will be completed as proposed or at all. The Transaction is an “arm’s length transaction” (as such term is defined in the policies of the TSXV as the Company is not a Related Party (as such term is defined in the policies of the TSXV) to 390.

The Transaction may require sponsorship under the policies of the TSXV unless an exemption or waiver from sponsorship is granted. NiCAN intends to apply for an exemption or waiver from sponsorship requirements of the TSXV in connection with the Transaction. There can be no assurance that such exemption or waiver will ultimately be granted.

Proposed Management and Board of Directors of the Resulting Issuer

Following the completion of the Transaction, the parties expect that the current board of directors and management of 390 will resign, and it is proposed that the following persons will be appointed as management of the Resulting Issuer, in the capacities set forth below. Brief biographies of the proposed nominees are as follows:

Brad Humphrey, Chief Executive Officer and Director

Mr. Humphrey has over 25 years of international mining experience. Prior to joining NiCAN, Mr. Humphrey was CEO of QMX Gold, which was acquired by Eldorado Gold. Prior to QMX, Mr. Humphrey worked for Morgan Stanley as an Executive Director and North American Precious Metals Analyst, where he was responsible for growing Morgan Stanley’s North American Gold research coverage. Mr. Humphrey was also a Managing Director and Head of Mining Research at Raymond James and covered precious metal equities at CIBC World Markets and Merrill Lynch. Mr. Humphrey has held a variety of mining industry roles from contract underground miner to CEO. Mr. Humphrey is currently on the board of Royal Fox Gold Inc.

Shaun Heinrichs, Chief Financial Officer

Mr. Heinrichs has over 20 years of experience in senior financial management and reporting, primarily in the mining industry. His career began at Ernst & Young, he subsequently held senior management roles in several public companies including serving as Chief Financial Officer of Veris Gold Corp., a precious metals producer listed in Canada and the US, from 2008 to 2015, and as the CFO of VMS Ventures Inc. from 2015 to 2016. Mr. Heinrichs also served as a director of Veris Gold Corp from 2012 to 2013. Presently Mr. Heinrichs is the CFO of Group Eleven Resources Corp., a zinc exploration company based in Ireland and 1911 Gold, a gold focused exploration company in Manitoba. Mr. Heinrichs is a Chartered Professional Accountant (CPA, CA) with the Institute of Chartered Accountants of British Columbia and holds a business degree from Simon Fraser University.

Wanda Roque, Corporate Secretary

Ms. Roque is a law clerk in the Province of Ontario. Ms. Roque has served as corporate secretary and has provided corporate and securities law clerk services to a number of public companies and reporting issuers since July 2007.

Michael Hoffman, Chairman and Director

Mr. Hoffman is currently Chair and Director at 1911 Gold as well as a director of Velocity Minerals, Silver X Mining and Fury Gold. He is a mining executive with over 35 years of experience including engineering, mine operations, corporate development, projects and construction. Mr. Hoffman also has direct northern Canadian mining experience including operations and projects. He is the former CEO of Crowflight Minerals, Kria Resources and Crocodile Gold.

Saga Williams, Director

Ms. Williams, LLB has worked in Indigenous communities in government and corporate roles in the capacity of legal counsel, negotiations and governance, and as a strategic advisor, for over 20 years. Ms. Williams has been on negotiation teams that have successfully settled over $1 billion in agreements and has worked on Indigenous community engagement and negotiations to support national energy and mining projects. Ms. Williams teaches at Osgoode Hall Law School as an Adjunct Professor and supports student led negotiations focussing on consultation, Indigenous rights and reconciliation. Over the last 25 years, she has also held many non-profit board positions. Ms. Williams is Anishinaabe, a member of Curve Lake First Nation, and is currently an elected official for her community.

Patrick Gleeson, Director

Mr. Gleeson was a corporate lawyer in Canada for almost twenty years, including working with Cassels, Brock & Blackwell LLP. He has taken over 40 companies public and served as general counsel, director and executive officer for several listed companies, from start-ups to those with billion-dollar market capitalizations. Presently, Mr. Gleeson is the president and founder of St. Peter’s Spirits Inc. (“St. Peter’s“), a socially conscious beverage company creating healthier-for-you drinks powered by plants. Prior to St. Peter’s, Mr. Gleeson founded IR Battery Resources & Processing, which consolidated the Delta Kenty Nickel project in northern Quebec, organized the first exploration program at Delta Kenty in over 15 years and ultimately sold the project to an international mining company.

Principal Securityholders

No Person or company will, to 390’s and NiCAN’s knowledge, beneficially own, directly or indirectly, or exercise control or direction over 10% or more of the outstanding Resulting Issuer Shares following the Transaction.

Qualified Person

Mr. Bill Nielsen P.Eng., a consultant to NiCAN, who is a Qualified Person under National Instrument 43-101, has reviewed and approved the scientific and technical information in this news release.

About NiCAN

NiCAN Limited is a private mineral exploration company, focused on high quality nickel-copper opportunities in stable jurisdictions on known mineral belts. The Company is actively exploring two projects, the Wine Property and the Pipy Project, both located in known mining jurisdictions in Manitoba Canada.

Contact Information:

1287390 B.C. Ltd.

James Ward, Director

416 897 2359

[email protected]

NiCAN Limited

Brad Humphrey

President and CEO

Phone: 416.565.4007

[email protected]

Shaun Heinrichs

CFO

Phone: 604.839.2788

[email protected]

Completion of the Transaction is subject to a number of conditions, including but not limited to, TSXV acceptance and if applicable, disinterested shareholder approval. Where applicable, the Transaction cannot close until the required shareholder approval is obtained. There can be no assurance that the Transaction will be completed as proposed or at all. Investors are cautioned that, except as disclosed in the filing statement to be prepared in connection with the Transaction, any information released or received with respect to the Transaction may not be accurate or complete and should not be relied upon. Trading in the securities of NiCAN and 390 should be considered highly speculative.

THE TSX VENTURE EXCHANGE INC. HAS IN NO WAY PASSED UPON THE MERITS OF THE PROPOSED TRANSACTION AND HAS NEITHER APPROVED NOR DISAPPROVED THE CONTENTS OF THIS NEWS RELEASE.

Further details of the transaction contemplated by the Definitive Agreement will be included in subsequent news releases and disclosure documents to be filed by 390.

Cautionary Note Regarding Forward-Looking Statements

The information contained herein contains “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements include, but are not limited to, statements with respect to: the terms and conditions of the proposed Transaction; the terms and conditions of the proposed Offering; use of proceeds from the Offering; future development plans; and the business and operations of the Resulting Issuer after the proposed Transaction. Forward-looking statements relate to information that is based on assumptions of management, forecasts of future results, and estimates of amounts not yet determinable. Any statements that express predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance are not statements of historical fact and may be “forward-looking statements.” Forward-looking statements are subject to a variety of risks and uncertainties which could cause actual events or results to differ from those reflected in the forward-looking statements, including, without limitation: risks related to failure to obtain adequate financing on a timely basis and on acceptable terms; risks related to the outcome of legal proceedings; political and regulatory risks associated with mining and exploration; risks related to the maintenance of stock exchange listings; risks related to environmental regulation and liability; the potential for delays in exploration or development activities or the completion of feasibility studies; the uncertainty of profitability; risks and uncertainties relating to the interpretation of drill results, the geology, grade and continuity of mineral deposits; risks related to the inherent uncertainty of production and cost estimates and the potential for unexpected costs and expenses; results of prefeasibility and feasibility studies, and the possibility that future exploration, development or mining results will not be consistent with the Company’s expectations; risks related to commodity price fluctuations; and other risks and uncertainties related to the Company’s prospects, properties and business detailed elsewhere in 390’s and the Company’s disclosure record. Should one or more of these risks and uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in forward-looking statements. Investors are cautioned against attributing undue certainty to forward-looking statements. These forward-looking statements are made as of the date hereof and 390 and the Company do not assume any obligation to update or revise them to reflect new events or circumstances. Actual events or results could differ materially from 390’s and the Company’s expectations or projections.

Not for distribution to United States news wire services or for dissemination in the United States.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/115523

Modern brands stake on influencer marketing, with 76% of users making a purchase after seeing a product on social media.The cryptocurrency industry is no exception to this trend. However, promoting crypto products through influencer marketing can be particularly challenging. Crypto influencers pose a significant risk to a brand’s reputation and ROI due to rampant scams. Approximately 80% of channels provide fake statistics, including followers counts and engagement metrics. Additionally, this niche is characterized by high CPMs, which can increase the risk of financial loss for brands.

In this article Nadia Bubennnikova, Head of agency Famesters, will explore the most important things to look for in crypto channels to find the perfect match for influencer marketing collaborations.

-

Comments

There are several levels related to this point.

LEVEL 1

Analyze approximately 10 of the channel’s latest videos, looking through the comments to ensure they are not purchased from dubious sources. For example, such comments as “Yes sir, great video!”; “Thanks!”; “Love you man!”; “Quality content”, and others most certainly are bot-generated and should be avoided.

Just to compare:

LEVEL 2

Don’t rush to conclude that you’ve discovered the perfect crypto channel just because you’ve come across some logical comments that align with the video’s topic. This may seem controversial, but it’s important to dive deeper. When you encounter a channel with logical comments, ensure that they are unique and not duplicated under the description box. Some creators are smarter than just buying comments from the first link that Google shows you when you search “buy YouTube comments”. They generate topics, provide multiple examples, or upload lists of examples, all produced by AI. You can either manually review the comments or use a script to parse all the YouTube comments into an Excel file. Then, add a formula to highlight any duplicates.

LEVEL 3

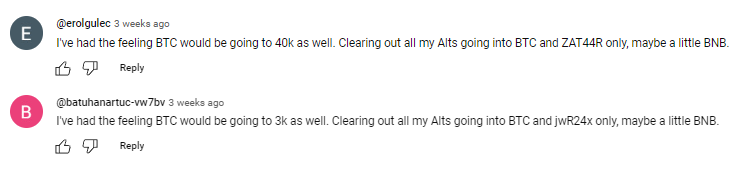

It is also a must to check the names of the profiles that leave the comments: most of the bot-generated comments are easy to track: they will all have the usernames made of random symbols and numbers, random first and last name combinations, “Habibi”, etc. No profile pictures on all comments is also a red flag.

LEVEL 4

Another important factor to consider when assessing comment authenticity is the posting date. If all the comments were posted on the same day, it’s likely that the traffic was purchased.

2. Average views number per video

This is indeed one of the key metrics to consider when selecting an influencer for collaboration, regardless of the product type. What specific factors should we focus on?

First & foremost: the views dynamics on the channel. The most desirable type of YouTube channel in terms of views is one that maintains stable viewership across all of its videos. This stability serves as proof of an active and loyal audience genuinely interested in the creator’s content, unlike channels where views vary significantly from one video to another.

Many unauthentic crypto channels not only buy YouTube comments but also invest in increasing video views to create the impression of stability. So, what exactly should we look at in terms of views? Firstly, calculate the average number of views based on the ten latest videos. Then, compare this figure to the views of the most recent videos posted within the past week. If you notice that these new videos have nearly the same number of views as those posted a month or two ago, it’s a clear red flag. Typically, a YouTube channel experiences lower views on new videos, with the number increasing organically each day as the audience engages with the content. If you see a video posted just three days ago already garnering 30k views, matching the total views of older videos, it’s a sign of fraudulent traffic purchased to create the illusion of view stability.

3. Influencer’s channel statistics

The primary statistics of interest are region and demographic split, and sometimes the device types of the viewers.

LEVEL 1

When reviewing the shared statistics, the first step is to request a video screencast instead of a simple screenshot. This is because it takes more time to organically edit a video than a screenshot, making it harder to manipulate the statistics. If the creator refuses, step two (if only screenshots are provided) is to download them and check the file’s properties on your computer. Look for details such as whether it was created with Adobe Photoshop or the color profile, typically Adobe RGB, to determine if the screenshot has been edited.

LEVEL 2

After confirming the authenticity of the stats screenshot, it’s crucial to analyze the data. For instance, if you’re examining a channel conducted in Spanish with all videos filmed in the same language, it would raise concerns to find a significant audience from countries like India or Turkey. This discrepancy, where the audience doesn’t align with regions known for speaking the language, is a red flag.

If we’re considering an English-language crypto channel, it typically suggests an international audience, as English’s global use for quality educational content on niche topics like crypto. However, certain considerations apply. For instance, if an English-speaking channel shows a significant percentage of Polish viewers (15% to 30%) without any mention of the Polish language, it could indicate fake followers and views. However, if the channel’s creator is Polish, occasionally posts videos in Polish alongside English, and receives Polish comments, it’s important not to rush to conclusions.

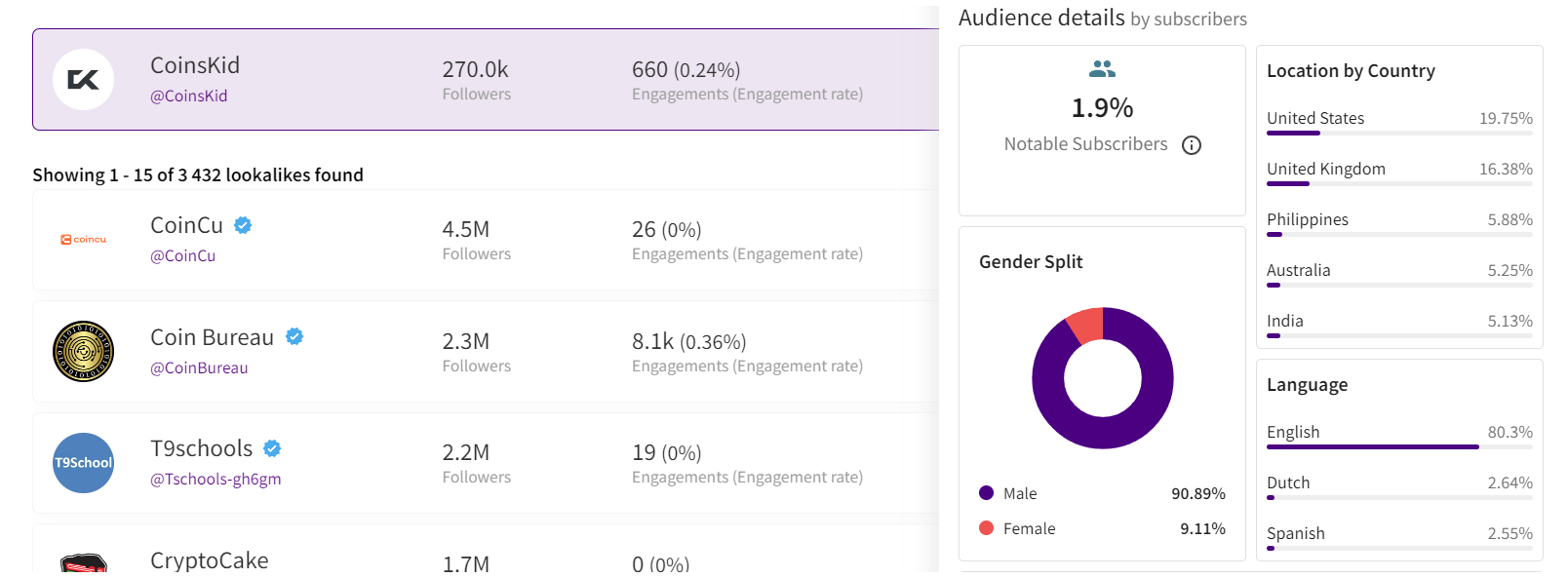

Example of statistics

Example of statistics

Wrapping up

These are the main factors to consider when selecting an influencer to promote your crypto product. Once you’ve launched the campaign, there are also some markers to show which creators did bring the authentic traffic and which used some tools to create the illusion of an active and engaged audience. While this may seem obvious, it’s still worth mentioning. After the video is posted, allow 5-7 days for it to accumulate a basic number of views, then check performance metrics such as views, clicks, click-through rate (CTR), signups, and conversion rate (CR) from clicks to signups.

If you overlooked some red flags when selecting crypto channels for your launch, you might find the following outcomes: channels with high views numbers and high CTRs, demonstrating the real interest of the audience, yet with remarkably low conversion rates. In the worst-case scenario, you might witness thousands of clicks resulting in zero to just a few signups. While this might suggest technical issues in other industries, in crypto campaigns it indicates that the creator engaged in the campaign not only bought fake views and comments but also link clicks. And this happens more often than you may realize.

Summing up, choosing the right crypto creator to promote your product is indeed a tricky job that requires a lot of resources to be put into the search process.

Author

Nadia Bubennikova, Head of agency at Famesters

The BIS, along with seven leading central banks and a cohort of private financial firms, has embarked on an ambitious venture known as Project Agorá.

Named after the Greek word for “marketplace,” this initiative stands at the forefront of exploring the potential of tokenisation to significantly enhance the operational efficiency of the monetary system worldwide.

Central to this pioneering project are the Bank of France (on behalf of the Eurosystem), the Bank of Japan, the Bank of Korea, the Bank of Mexico, the Swiss National Bank, the Bank of England, and the Federal Reserve Bank of New York. These institutions have joined forces under the banner of Project Agorá, in partnership with an extensive assembly of private financial entities convened by the Institute of International Finance (IIF).

At the heart of Project Agorá is the pursuit of integrating tokenised commercial bank deposits with tokenised wholesale central bank money within a unified, public-private programmable financial platform. By harnessing the advanced capabilities of smart contracts and programmability, the project aspires to unlock new transactional possibilities that were previously infeasible or impractical, thereby fostering novel opportunities that could benefit businesses and consumers alike.

The collaborative effort seeks to address and surmount a variety of structural inefficiencies that currently plague cross-border payments. These challenges include disparate legal, regulatory, and technical standards; varying operating hours and time zones; and the heightened complexity associated with conducting financial integrity checks (such as anti-money laundering and customer verification procedures), which are often redundantly executed across multiple stages of a single transaction due to the involvement of several intermediaries.

As a beacon of experimental and exploratory projects, the BIS Innovation Hub is committed to delivering public goods to the global central banking community through initiatives like Project Agorá. In line with this mission, the BIS will soon issue a call for expressions of interest from private financial institutions eager to contribute to this ground-breaking project. The IIF will facilitate the involvement of private sector participants, extending an invitation to regulated financial institutions representing each of the seven aforementioned currencies to partake in this transformative endeavour.

Source: fintech.globa

The post Central banks and the FinTech sector unite to change global payments space appeared first on HIPTHER Alerts.

TD Bank has inked a multi-year deal with Google Cloud as it looks to streamline the development and deployment of new products and services.

The deal will see the Canadian banking group integrate the vendor’s cloud services into a wider portion of its technology solutions portfolio, a move which TD expects will enable it “to respond quickly to changing customer expectations by rolling out new features, updates, or entirely new financial products at an accelerated pace”.

This marks an expansion of the already established relationship between TD Bank and Google Cloud after the group previously adopted the vendor’s Google Kubernetes Engine (GKE) for TD Securities Automated Trading (TDSAT), the Chicago-based subsidiary of its investment banking unit, TD Securities.

TDSAT uses GKE for process automation and quantitative modelling across fixed income markets, resulting in the development of a “data-driven research platform” capable of processing large research workloads in trading.

Dan Bosman, SVP and CIO of TD Securities, claims the infrastructure has so far supported TDSAT with “compute-intensive quantitative analysis” while expanding the subsidiary’s “trading volumes and portfolio size”.

TD’s new partnership with Google Cloud will see the group attempt to replicate the same level of success across its entire portfolio.

Source: fintechfutures.com

The post TD Bank inks multi-year strategic partnership with Google Cloud appeared first on HIPTHER Alerts.

-

Fintech5 days ago

Fintech5 days agoHow to identify authenticity in crypto influencer channels

-

Latest News5 days ago

HSBC-backed fintech Monese is considering splitting its operations as it grapples with increasing losses.

-

Latest News4 days ago

EverBank has announced a groundbreaking partnership with Finzly, poised to revolutionize payment processing.

-

Latest News4 days ago

FinTech leaders express caution regarding the promises made in #Budget2024 concerning open banking, stating that the “devil is in the details.”

-

Latest News4 days ago

Gotion High-tech’s operating profit up 391% in 2023, nearly RMB 2.8 billion invested in R&D for the year

-

Latest News4 days ago

Aurionpro Solutions acquires Arya.ai, to power next generation Enterprise AI platforms for Financial Institutions

-

Latest News5 days ago

Wells Fargo, a leading financial institution, is set to revolutionize its trade finance operations by incorporating artificial intelligence (AI) technology through its collaboration with TradeSun.

-

Latest News4 days ago

Latvian Fintech inGain Raises €650,000 for No-Code SaaS Loan Management System