Fintech

TRU Precious Metals Drills More Gold at Golden Rose Project and Releases Woods Lake Gold Zone Model

Toronto, Ontario–(Newsfile Corp. – April 7, 2022) – TRU Precious Metals Corp. (TSXV: TRU) (OTCQB: TRUIF) (FSE: 706) (“TRU” or the “Company”) is pleased to announce new assay results from an additional 5 of the 22 holes completed during its 2021 winter drill program at its flagship Golden Rose Project in Central Newfoundland (“Golden Rose”). In addition, TRU is releasing a longitudinal cross section model (see Figure 1) of the Woods Lake Gold Zone (“Woods Lake”), which was the primary focus of that drill program.

TRU has now reported on 16 holes in total, with assays from the remaining 6 holes still pending. This includes 4 holes at the King George IV area (“KG4”) and 2 holes at Woods Lake. Reported drilling results at Woods Lake now define a primary gold zone that is 800 metres (m) in strike length (from holes WL-21-06 to WL-21-14) and is open both along strike and at depth.

Highlights

-

1.51 grams per tonne (g/t) gold over 11m from 71.0m down hole in DDH WL-21-05, within a broader interval of 0.59 g/t gold over 38m from 49.0m depth down hole. (see Table 1)

-

Woods Lake has now been intersected in drilling over 800m along strike. It remains open for expansion along strike and down dip, and the recent drilling has begun to outline a potential southwest and southeast plunge.

TRU Co-Founder and CEO Joel Freudman commented: “This early drilling success at Golden Rose only scratches the surface of the substantial potential and underexplored nature of this property. Woods Lake was the sole previously known gold zone at Golden Rose, and we are pleased with our results there to date, yet we expect numerous additional mineralized areas remain to be discovered and or proved up across the property. As such, we are also excited about our 2022 work and exploration program already underway at Golden Rose. We are grateful to our exploration team, thank them for their hard work so far and look forward to their ongoing contributions to TRU’s continued exploration success. We remain focused on executing our exploration strategy and will continue to deliver meaningful progress and results in the coming months.”

The drill program at Golden Rose consisted of a total of 22 HQ diamond drill holes for a total of 4,102.7m, covering both Woods Lake and KG4 . Golden Rose is a regional-scale 236 square kilometre (km) land package, including 45 km of strike length along the deposit-bearing Cape Ray – Valentine Lake Shear Zone, and is located directly between Marathon Gold’s Valentine Gold Project and Matador Mining’s Cape Ray Gold Project.

Barry Greene, VP of Property Development and Director of TRU, added: “Our drill data continues to successfully define a potential bulk tonnage gold zone at Woods Lake. As we input infill drilling assays to our gold zone model, it points to a zone that appears to plunge in two directions. This will provide additional vectors in which to target deeper drilling. We feel this is further evidence of the inherent value at Golden Rose and are, therefore, evermore excited about our current property-wide work program underway.”

Table 1 – Woods Lake Uncut Assay Highlights.

| Hole No. | From (m) | To (m) | Interval (m) | Au (g/t) | Zone |

| WL-21-05 | 49.00 | 87.00 | 38.00 | 0.59 | Woods Lake |

Including |

71.00 |

82.00 |

11.00 |

1.51 |

|

| WL-21-13 | 131.00 | 140.00 | 9.00 | 0.34 |

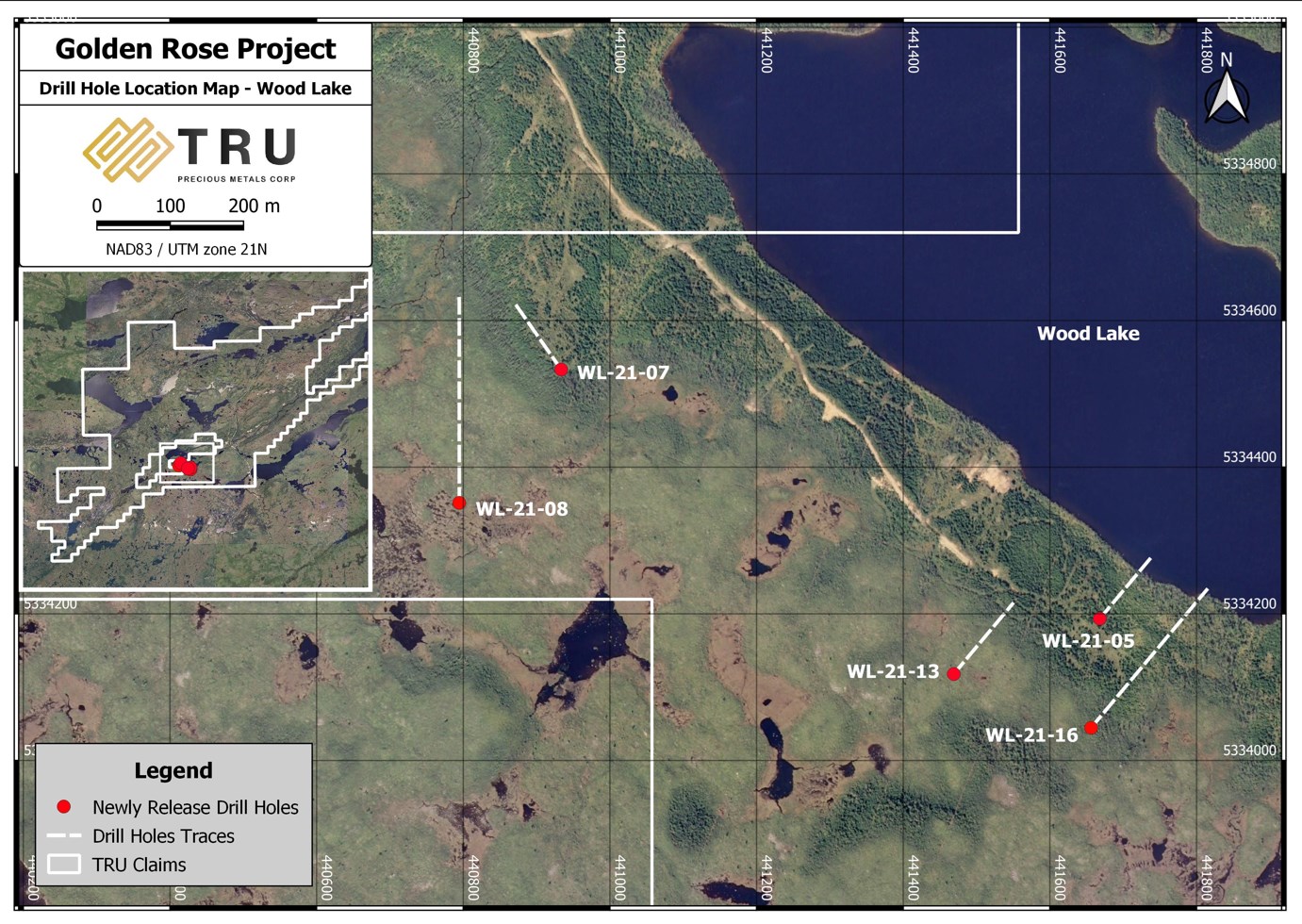

Figure 2 – Woods Lake Drill Hole Location Map

To view an enhanced version of Figure 2, please visit:

https://orders.newsfilecorp.com/files/5993/119551_9bdc24b61432d89c_002full.jpg

Table 2 – Woods Lake Collar Details.

| Hole No. | Azimuth (°) | Dip (°) | Length (m) | UTM E | UTM N |

| WL-21-05 | 40 | 45 | 151 | 441668 | 5334194 |

| WL-21-07 | 325 | 68 | 299 | 440934 | 5334533 |

| WL-21-08 | 0 | 45 | 401 | 440795 | 5334351 |

| WL-21-13 | 40 | 45 | 176 | 441469 | 5334118 |

| WL-21-16 | 40 | 45 | 347 | 441656 | 5334045 |

Drill holes WL-21-07 and WL-21-08 were exploratory scout holes testing an historical IP anomaly to the northwest of Woods Lake and did not return significant gold values. WL-21-16 also did not return significant gold values.

Separately, the Company reports that certain of its directors, officers, employees, and consultants have voluntarily forfeited an aggregate of 2,590,000 stock options with exercise prices above $0.25 per share, in order to streamline the Company’s capital structure.

Drilling Quality Assurance/Quality Control (“QA/QC”)

All HQ core is geotechnically measured for RQD’s, logged and marked for sampling. The core is then cut by Company personnel, with half put into bags with unique sample tags for identification while the other half is retained for reference. The bags are sealed with a security tag and are then transported directly to the lab by TRU staff. All rock samples are analyzed at Eastern Analytical Ltd. (“Eastern Analytical”) of 403 Little Bay Road, Springdale, NL, a commercial laboratory that is ISO/IEC 17025 accredited and independent of TRU. Eastern Analytical pulverized 1,000 grams of each sample to 95% < 89 μm. Samples are analyzed using fire assay (30g) with AA finish and an ICP-34, four acid digestion followed by ICP-OES analysis. All samples with visible gold or assaying above 1.00 g/t Au are further assayed using metallic screen to mitigate the presence of the nugget effect of coarse gold. Standards and blanks are inserted at defined intervals for QA/QC purposes by the Company as well as Eastern Analytical. True widths for reported intervals have yet to be determined. The TRU exploration program design is consistent with industry best practices and the program is carried out by qualified persons employing a QA/QC program consistent with National Instrument 43-101.

Qualified Person

Barry Greene, P.Geo. (NL) is a qualified person as defined by National Instrument 43-101 and has reviewed and approved the contents and technical disclosures in this press release. Mr. Greene is a director and officer of the Company and owns securities of the Company.

About TRU Precious Metals Corp.

TRU is drilling for gold in the highly prospective Central Newfoundland Gold Belt and has an option with TSX-listed Altius Minerals to purchase 100% of the Golden Rose Project. Golden Rose is a regional-scale 236 km2 land package, including 45 kilometres of strike length along the deposit-bearing Cape Ray – Valentine Lake Shear Zone directly between Marathon Gold’s Valentine Gold Project and Matador Mining’s Cape Ray Gold Project. TRU’s common shares trade on the TSX Venture under the symbol “TRU”, on the OTCQB Venture under the symbol “TRUIF”, and on the Frankfurt exchange under the symbol “706”.

TRU is a portfolio company of Resurgent Capital Corp. (“Resurgent”), a merchant bank providing venture capital markets advisory services and proprietary financing. Resurgent works with promising public and pre-public micro-capitalization companies listing on Canadian stock exchanges. For more information on Resurgent and its portfolio companies, please visit Resurgent’s website at https://www.resurgentcapital.ca/ or follow Resurgent on LinkedIn at https://ca.linkedin.com/company/resurgent-capital-corp.

For further information about TRU, please contact:

Joel Freudman

Co-Founder & CEO

TRU Precious Metals Corp.

Phone: 1-855-760-2TRU (2878)

Email: [email protected]

To connect with TRU via social media, below are links:

Twitter

https://twitter.com/corp_tru

LinkedIn

https://www.linkedin.com/company/tru-precious-metals-corp

YouTube

https://www.youtube.com/channel/UCHghHMDQaYgS1rDHiZIeLUg/

Acknowledgement

TRU would like to thank the Government of Newfoundland and Labrador for its past financial support through the Junior Exploration Assistance Program.

Cautionary Statements

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

This press release contains certain forward-looking statements, including those relating to exploration plans and drill program results at Golden Rose. These statements are based on numerous assumptions regarding Golden Rose and the Company’s drilling program and results that are believed by management to be reasonable in the circumstances, and are subject to a number of risks and uncertainties, including without limitation: mineralization hosted on adjacent and/or nearby properties is not necessarily indicative of mineralization hosted on Golden Rose; the exploration potential of Golden Rose and the nature and style of mineralization at Golden Rose; risks inherent in mineral exploration activities; volatility in precious metals prices; and those other risks described in the Company’s continuous disclosure documents. Actual results may differ materially from results contemplated by the forward-looking statements herein. Investors and others should carefully consider the foregoing factors and should not place undue reliance on such forward-looking statements. The Company does not undertake to update any forward-looking statements herein except as required by applicable securities laws.

{kind=link}

Fintech

Asian Financial Forum held next week as the region’s first major international financial assembly of 2025

The 18th Asian Financial Forum 2025 (AFF), co-organised by the Government of the Hong Kong Special Administrative Region (HKSAR) and the Hong Kong Trade Development Council (HKTDC), will be held at the Hong Kong Convention and Exhibition Centre (HKCEC) on 13 and 14 January (Monday and Tuesday). As the region’s first major international financial conference in 2025, the forum will examine the landscape for new business opportunities in various industries and regions in the coming year and promote global cooperation, and is expected to attract more than 3,600 finance and business heavyweights.

Themed “Powering the Next Growth Engine”, the AFF will bring together more than 100 global policymakers, business leaders, financial experts and investors, entrepreneurs, tech companies and economists to share their views on the shifting global economic landscape and financial ecosystem. These industry experts will dissect the risk management strategy, discover new business opportunities, and explore how Hong Kong can seek breakthroughs in a period of change.

First flagship financial event to showcase Hong Kong’s financial strengths

Launched in 2007, the AFF has become a flagship financial event for Hong Kong and the broader region, highlighting the city’s pivotal role as a globally renowned financial hub with a highly competitive economic and business environment. Amid a rapidly changing global macroeconomic landscape, and shifts in geopolitical dynamics and monetary policies, Hong Kong’s financial services sector continues to leverage its strengths across various domains, drawing on its world-class business infrastructure and robust regulatory regime to help drive cooperation and mutual success across Asia and around the world.

Christopher Hui, Secretary for Financial Services and the Treasury of the HKSAR Government, said: “Hong Kong’s financial market went through a lot of reforms and innovation last year. We have also launched a roadmap on sustainability disclosure in Hong Kong and issued a policy statement on responsible application of artificial intelligence in the financial market with a view to boosting green finance and sustainable financing. The upcoming Asian Financial Forum will gather the top-tier of the financial and various sectors from all around the world, the Mainland and in Hong Kong and hence is the perfect occasion for us to showcase to the world the new momentum and latest advantages of Hong Kong in the financial realm. Participants will also have a chance to learn more about how Hong Kong can partner with them to explore new collaborations and development areas while expanding their network here.”

Luanne Lim, Chairperson of the AFF Steering Committee and Chief Executive Officer, Hong Kong, of HSBC, said: “The global economy faces greater uncertainties in 2025 compared to 2024. However, robust growth in India and ASEAN nations, combined with increased policy support from Mainland China, is expected to keep Asia’s (ex-Japan) GDP growth at a strong 4.4%, well above the global average of 2.7%.” Against this backdrop, this year’s Asia Financial Forum is aptly themed “Powering the Next Growth Engine” and will focus on high-potential markets such as ASEAN, the Middle East (particularly the Gulf Cooperation Council countries), and the role that Hong Kong can play. Ms Lim said Hong Kong’s unique role as a bridge between the mainland and international markets allows it to support mainland enterprises expanding globally. She added that Hong Kong is committed to attracting global talent and investors, driving growth for both mainland and international businesses.

Patrick Lau, HKTDC Deputy Executive Director, said: “As we move into the new year, different economies around the world are facing challenges in maintaining economic growth. As an international financial centre, Hong Kong is playing an important role both as a ‘super-connector’ and a ‘super value-adder’ to link the world, enabling investors and fundraisers to leverage the city’s professional services and investment platforms to facilitate collaboration and create business opportunities. This year’s forum not only brings together heavyweight speakers and thought leaders but also builds on the success of previous years to provide a business platform for international participants, promoting financial and business cooperation and working together to launch new engines for growth.”

Exploring new trends as the world’s economic centre of gravity continues its shift east

Reflecting on a trend where the world’s economic centre of gravity continues to take an eastward shift, Christopher Hui will host two plenary sessions on emerging prospects in the region on the first day of the forum (13 January). The morning session of Plenary Session I will feature H.E. Adylbek Kasymaliev, Prime Minister of Kyrgyzstan, finance ministers from countries such as Pakistan and Luxembourg, and Yoshiki Takeuchi, Deputy Secretary-General of the Organisation for Economic Co-operation and Development (OECD), who together will explore the financial policy outlook for 2025. In the afternoon, Plenary Session II will bring together leaders from multilateral organisations to share their views on the role of multilateral cooperation in regional economic development. Speakers will include Roberta Casali, Vice-President, Finance and Risk Management, Asian Development Bank; Jin Liqun, President and Chair of the Asian Infrastructure Investment Bank (AIIB); and Satvinder Singh, Deputy Secretary-General for ASEAN Economic Community, Association of Southeast Asian Nations (ASEAN). Moreover, a new session, the Gulf Cooperation Council Chapter, will bring together HE Jasem Mohamed AlBudaiwi, Secretary General of the Gulf Cooperation Council (GCC), speakers from the Middle East and local experts to discuss prospects in fostering financial cooperation and investment between the member states of the GCC and Hong Kong.

Also on the first day, Eddie Yue, Chief Executive of the Hong Kong Monetary Authority, will host the Policy Dialogue session with speakers including European representatives such as Philip Lane, Chief Economist and Member of the Executive Board of the European Central Bank, and Dr Olli Rehn, Governor of the Bank of Finland. The discussion will explore the opportunities and challenges arising from the global shift towards more accommodative monetary policies and national authorities’ strategic deployment of measures to revitalise their economies and accelerate growth through innovation.

The panel discussion on China Opportunities returns this year with senior figures invited to analyse investment prospects under China’s commitment to technological innovation and its impact on global business. The panellists included Li Yimei, Chief Executive Officer of China Asset Management; and Ken Wong, Executive Vice President of Lenovo and President of Lenovo Solutions & Services Group.

Top economist and leading AI expert take the stage at keynote luncheons

Another highlight of this year’s AFF will be the two keynote luncheons featuring thematic speeches by two distinguished guests: Prof Justin Lin Yifu, Chief Economist and Senior Vice President of the World Bank (2008-2012), and Prof Stuart Russell, Co-chair of the World Economic Forum Council on AI. These two prominent figures will dissect the evolution of the global economic landscape amid changing international dynamics, and examine how artificial intelligence (AI) is emerging as a new driving force for rapid global economic growth respectively.

Exploring hot topics in the financial and economic sectors

The afternoon panel discussion, Global Economic Outlook, will feature a special address from Liu Haoling, Vice Chairman, President and Chief Investment Officer, China Investment Corporation. The panel will analyse international economic trends and provide insights into business opportunities and wealth accumulation in emerging industries and regions in 2025.

Other sessions titled Global Spectrum, Dialogues for Tomorrow and Thematic Workshop will feature in-depth discussions focusing on the latest industry trends, including AI, Web 3.0, sustainability, philanthropy and family offices. As AI becomes increasingly widespread and diversified in its societal applications, the second day of the forum will introduce a special session, Dialogue with Kai-Fu Lee, in which Dr Kai-Fu Lee, Chairman of Sinovation Ventures, will discuss the transformative power of AI and its impact on technological advancements in the global business ecosystem.

Exploring the impact of sustainable disclosure on investment strategies

Sustainable finance and environmental, social and governance (ESG) considerations have become an irreversible global trend. In 2025, Hong Kong is set to fully align its regulatory framework with the sustainability disclosure standard of the International Sustainability Standards Board (ISSB). Sue Lloyd, Vice Chair of the ISSB, will join other experts in discussing how adopting international financial sustainability disclosure standards can strengthen market confidence in Hong Kong’s capital markets, address post-COP29 implementation in Asia, and share strategies for sustainable investing across three separate sessions. In addition, the Breakfast Panel on the second day will focus on the flows of transition finance in shaping a sustainable future in the Greater Bay Area and beyond. Furthermore, the HKTDC has partnered with EY to conduct a joint market survey on sustainable development, aiming to explore the views and practices of Asian businesses and investors on topics such as sustainability reporting, sustainable finance and preparations for dealing with climate change. The results of the survey will be unveiled on the first day of the forum.

Expanding cross-border opportunities through the HK global investment platform

As a key element of this year’s forum, AFF Deal-making offers one-on-one matching services for project owners and investors. More than 270 investors and 560 projects are expected to participate, with investment opportunities across industries such as environmental, energy, clean technology, food and agriculture tech, healthcare tech, fintech and deep technology. The exhibition sections of the AFF – Fintech Showcase, InnoVenture Salon, FintechHK Startup Salon and Global Investment Zone – will attract more than 130 local and global exhibitors, international financial institutions, technology companies, start-ups, investment promotion agencies and sponsors, including Knowledge Partner EY, HSBC, Bank of China (Hong Kong), Standard Chartered Bank, UBS, Prudential, China International Capital Corporation (CICC), Huatai International and more. Notably, the InnoVenture Salon will provide a platform for more than 100 start-ups to showcase innovative technologies in a variety of fields such as finance, regulation, sustainability, health and agriculture, supported by more than 110 Investment Mentors and Community Partners.

IFW 2025 creates synergies with AFF to boost mega event economy

International Financial Week (IFW) 2025 runs from 13 to 17 January with the AFF as its highlight event. This year’s IFW will feature more than 20 partner events, covering a wide range of global financial and business topics, including private equity, family offices, net-zero investing and generative AI. As the region’s first major financial event of the year, the AFF attracts top global enterprises and leaders to Hong Kong, creating connections between capital and opportunities. The forum assists industry professionals in seizing opportunities in the new year and helps promote the mega event economy in Hong Kong.

This year, the AFF has collaborated with various organisations to provide special travel, dining and shopping discounts and privileges for overseas participants joining the event. Activities include Peak Tram and Sky Terrace trips, the iconic Aqua Luna red-sail junk boat, and guided tours of Man Mo Temple and Tai Kwun arranged by the Hong Kong Tourism Board. Participants can also enjoy dining discounts and guided tours from the Lan Kwai Fong Group, as well as the Winter Wonderland at the Hong Kong Jockey Club’s Happy Wednesday at Happy Valley Racecourse, all designed to immerse overseas visitors in the vibrancy and diversity of Hong Kong.

The post Asian Financial Forum held next week as the region’s first major international financial assembly of 2025 appeared first on News, Events, Advertising Options.

As we close out 2024, the fintech industry continues to deliver headlines that underscore its dynamism and innovation. From IPO aspirations to groundbreaking regulatory milestones, today’s updates highlight the transformative power of fintech partnerships, regulatory evolution, and disruptive technologies. Here’s what you need to know.

Chime’s Quiet Step Toward Public Markets

Chime, the U.S.-based financial technology startup best known for its digital banking services, has taken a significant step by filing confidential paperwork for an initial public offering (IPO). As one of the most valuable private fintechs in the U.S., Chime’s move could potentially signal a renewed appetite for fintech IPOs in a market that has been cautious following fluctuating valuations across the tech sector.

With a valuation that reportedly exceeded $25 billion in its last funding round, Chime’s IPO could set a new benchmark for the industry. Observers note that its strong customer base and revenue growth may make it an appealing choice for investors seeking to capitalize on the digital banking boom. However, the timing and success of the IPO will depend on broader market conditions and the regulatory landscape.

Source: Bloomberg

ZBD’s Pioneering Achievement: EU MiCA License Approval

ZBD, a fintech company specializing in Bitcoin Lightning network solutions, has made history by becoming the first to secure an EU MiCA (Markets in Crypto-Assets Regulation) license. This landmark approval by the Dutch regulator positions ZBD at the forefront of compliant crypto-fintech operations in Europe.

MiCA, which aims to harmonize the regulatory framework for crypto-assets across the EU, has been a focal point for industry players aiming to establish legitimacy and expand their offerings. ZBD’s achievement not only validates its operational rigor but also sets a precedent for other fintech firms navigating the evolving regulatory landscape.

Industry insiders view this as a strategic advantage for ZBD as it broadens its footprint in Europe. By leveraging its regulatory approval, the company can accelerate its product deployment and establish trust with institutional and retail users alike.

Source: Coindesk, PR Newswire

The Fintech-Credit Union Synergy: A Blueprint for Innovation

The convergence of fintechs and credit unions continues to reshape the financial services ecosystem. Collaborative initiatives, such as the one highlighted in the recent partnership between fintech innovators and credit unions, are proving to be a potent force in delivering tailored financial solutions.

This “dream team” approach allows credit unions to leverage fintech’s technological expertise while maintaining their community-focused ethos. Key areas of collaboration include digital payments, personalized financial management tools, and enhanced loan processing capabilities. These partnerships not only enhance member engagement but also enable credit unions to remain competitive in an increasingly digital-first financial environment.

Industry analysts emphasize that such collaborations underscore a broader trend of traditional financial institutions embracing fintech-driven solutions to bridge service gaps and foster innovation.

Source: PYMNTS

Tackling Student Loan Debt: A Fintech’s Mission

Student loan debt remains a pressing issue for millions of Americans, and a Rochester-based fintech aims to offer relief through its cloud-based platform. This innovative solution is designed to simplify loan management and provide borrowers with actionable insights to reduce their debt burden.

The platform’s features include repayment optimization tools, personalized financial education, and seamless integration with loan servicers. By addressing the complexities of student loan management, this fintech is empowering borrowers to make informed decisions and achieve financial stability.

As the student loan crisis continues to evolve, solutions like this highlight the critical role fintech can play in addressing systemic financial challenges while fostering financial literacy and inclusion.

Source: RBJ

Industry Implications and Takeaways

Today’s updates underscore several key themes shaping the fintech landscape:

- Regulatory Milestones: ZBD’s MiCA license approval exemplifies the importance of regulatory compliance in unlocking growth opportunities.

- Strategic Partnerships: The collaboration between fintechs and credit unions demonstrates the value of combining technological innovation with traditional financial models to drive customer-centric solutions.

- Market Opportunities: Chime’s IPO move reflects a potential revival in fintech public offerings, signaling confidence in the sector’s long-term prospects.

- Social Impact: Fintech’s ability to tackle systemic issues, such as student loan debt, showcases its role as a force for positive change.

The post Fintech Pulse: Your Daily Industry Brief (Chime, ZBD, MiCA) appeared first on News, Events, Advertising Options.

Leading global payments platform SPAYZ.io has confirmed it will be attending iFX EXPO Dubai 2025 on 14 to 16 January. Exhibiting at Stand 64 at Trade Centre Dubai, SPAYZ.io’s team of professionals will be on hand providing live demonstrations of its renowned payment services for payment providers. Attendees will also receive exclusive insight into SPAYZ.io’s plans for 2025 alongside early early access to its upcoming plans for the new year.

SPAYZ.io delivers a host of payment solutions that leverage the latest technological innovations and open access to the fastest growing emerging markets across Africa, Europe and Asia. Over the past year, there has been huge demand for its Open Banking and local payment method services, alongside bank transfers, mass payouts, online banking and e-wallets.

Yana Thakurta, Head of Business Development at SPAYZ.io commented: “We look forward to once again participating at iFX Dubai to expand our network of partners and clients. It’s a fantastic way to kick off the year, connecting with thousands of industry leaders from FOREX platforms to trading companies, and everything in between.

“Our key goal for iFX Dubai EXPO 2025 is to expand our portfolio of solutions and geographies. We’re using this as an opportunity to partner with like-minded entities who share our ambition to provide payment solutions that are truly global.”

Come meet SPAYZ.io’s team at the Trade Centre Dubai at Stand 64. You can also book a meeting slot with a member of a team.

The post SPAYZ.io prepares for iFX EXPO Dubai 2025 appeared first on News, Events, Advertising Options.

-

Fintech PR7 days ago

Fintech PR7 days agoBybit x Block Scholes Report: BTC Options Steady with Call-Put Parity, ETH Braces for Short-Term Volatility

-

Fintech PR7 days ago

Fintech PR7 days agoArtificial Intelligence (AI) in Trading Market to Reach USD 35 Billion by 2030, Growing at a 10% CAGR | Valuates Reports

-

Fintech3 days ago

Fintech3 days agoAsian Financial Forum held next week as the region’s first major international financial assembly of 2025

-

Fintech PR3 days ago

Fintech PR3 days agoOWIT Global Provides Alternative Delivery Models that Adapt to the Continuously Evolving Data Security Demands of the Industry

-

Fintech PR4 days ago

Fintech PR4 days agoHyundai Motor Group Executive Chair Euisun Chung Outlines 2025 Vision Driven by Commitment to Innovation, Overcoming Challenges, and Creating Opportunities in New Year’s Message

-

Fintech PR4 days ago

Fintech PR4 days agoZoomlion Accelerates Global Expansion with Localized Innovations in Saudi Arabia

-

Fintech PR5 days ago

Fintech PR5 days agoPayroll Service Market Anticipates Strong Growth Amid Rising Automation Demand

-

Fintech PR1 day ago

Fintech PR1 day agoClear Channel Outdoor Holdings, Inc. to Sell its Europe-North Segment to a subsidiary of Bauer Media Group for $625 Million