Fintech

Raffles Financial Corporate Update

Singapore, Singapore–(Newsfile Corp. – December 27, 2022) – Raffles Financial Group Limited (CSE: RICH) (FSE: 4VO) (OTC: RAFFF) (“RFG” or the “Company“) This is to give shareholders a corporate update of the Company and its only operating subsidiary, Raffle Financial Pte Ltd (“RFP“).

Disclosure of Financial Information for FY2022 of the Major Operating Subsidiary

The audit on the only operating subsidiary of RFG, Raffles Financial Private Limited (“RFP“), which is performed by an auditor in Singapore, is completed and its audit report for the financial year ended June 30, 20221 (“FY2022“) is issued to the Board. RFG believes RFP’s audited financial information is relevant information for our shareholders to understand the financial performance of the Group. Therefore, although the RFG’s audit is still pending, the Board wishes to present the following management discussion and analysis of the key financial performance of RFP to our shareholders.

| Statement of Comprehensive Income | (“FY2022”) | (“FY2021”) | ||||

| (Presented in Singapore Dollars) | July 1, 2021 | July 1, 2020 | ||||

| to | to | |||||

| June 30, 2022 | June 30, 2021 | |||||

| SGD | SGD | |||||

| Revenue | – | 4,999,880 | ||||

| Other income | 5,266 | 9,161,901 | ||||

| Expenses: | ||||||

| Staff and contract officers’ cost | 519,618 | 681,114 | ||||

| Office Rental | 33,336 | 83,766 | ||||

| Professional fee | 53,671 | 39,739 | ||||

| Listing fee | – | 7,177 | ||||

| Realised loss / (gain) on disposal of subsidiary | 151,714 | (931,029) | ||||

| Others – waiver of an intercompany loan receivables | 58,299 | 2,968,000 | ||||

| Loss allowance on other receivables – net | 2,988,736 | 4,102,796 | ||||

| Other expenses | 40,215 | 165,550 | ||||

| 3,845,589 | 7,117,113 | |||||

| (Loss) / Profit before income tax | (3,840,323 | ) | 7,044,668 | |||

| Income tax expense | 180,920 | 849,980 | ||||

| (Loss) / Profit after income tax | (4,021,243 | ) | 6,194,688 | |||

| Other Comprehensive Income: | ||||||

| Items that will not be reclassified subsequently to profit or loss: Financial assets, at FVOCI |

||||||

| – Fair value (loss) / gain – equity investments | (4,613,046 | ) | 265,208 | |||

| Total comprehensive (loss) / income | (8,634,289 | ) | 6,459,896 |

The Company’s major and only operating subsidiary RFP is the sole business operating unit and revenue contributor of the Group. In FY2022, RFP did not record any revenue (FY2021: 4,999,880) from the three major service segments, namely (i) Re-structuring and Corporate Finance Advisory service with service fee (FY2021: S$2,000,000 rendered at a point in time); (ii) IPO and Global Fund-Raising Advisory service with service fee (FY2021: S$2,000,000 rendered over time), and (iii) licensing service with licensing fee (FY2021: S$999,880 rendered over time). It was attributable to the following factors:

-

The prolonged COVID-19 pandemic and its variants outbreak caused China and Hong Kong, where were the major regions RFP operated, upheld strict travel restrictions, containment measures and lockdown. As a result, RFP was unable to source and serve its customers in its principal operating locations;

-

The COVID-19 pandemic also severely hit the IPO climate resulting in the mood and confidence of clients to hold back its IPO and fundraising plans till such situation turnarounds;

-

The public health, global economic conditions and geopolitical issues affected the overall Asia financial market including corporate finance, IPO and investment banking industry in the past two years. As arranging and financing deals drying up, the whole capital market and investment banking industry have been down severely evidenced by the circumstance that large investment banks like Morgain Stanley, Goldman Sachs and Credit Suisse were firming up plans to cut jobs and reduce team size in Asian region.

Amid the challenges, RFG has been maintaining the prospective client relationship and training regional representatives to get their mandates for advisory services when the market condition improves.

There was a significant decrease in expenses in FY2022 over FY2021 from S$7,117,113 to S$3,845,589 which was mainly due to the stringent cost control measure RFP put under the challenging business environment.

Among the expenses –

-

RFP recorded a loss allowance on other receivable (net) of S$2,988,736 in FY2021. This was a one-off accounting provision made for aged receivables with slow repayment in accordance with the prudence principle under the accounting standards. The subject receivables were due from an unrelated third party in connection to sales of long-term investments in equity instruments made in FY2021. Whereas receivables were written off, RFP continues to take recovery action against the debtor. Where recoveries of receivables exceed the written-off amount, the excess will be recognised in profit or loss as an income in the relevant financial period;

-

The realised loss on disposal of subsidiary of S$151,714 in FY2022 was largely derived from a disposal of 100% equity interest in an inactive subsidiary in Switzerland. The disposal resulted in a loss of S$151,658 in RFP’s book. However, on the other hand, the disposal also resulted in a gain of S$131,453 as the subsidiary had transferred its whole bank balance of S$131,453 to RFG right before the disposal which was recognised as an other income. Therefore, the loss arising from the disposal at consolidation level was immaterial;

-

There was a waiver of an intercompany loan receivables from a subsidiary of RFP amounted to S$58,299. The waiver amount represented the advance made to the subsidiary for paying its business expenses, which was eventually borne by RFP upon the disposal of the subsidiary.

From an operation perspective, RFP recorded a net operating loss after tax of S$4,021,243 in FY2022 compared with the net profit after tax of S$6,194,688.

To conclude, RFP recorded a total comprehensive loss of S$8,634,290 in FY2022 compared with the total comprehensive income of S6,459,896 in FY2021. The loss was mainly attributable to the net operating loss as described above and an unrealised fair value loss on equity investments of S$4,613,046 (FY2021: an unrealised fair value gain of 265,208). The unrealised fair value loss was provided for on paper under prudence practice, considering the share prices of our listed equity instruments, like many other listed entities on major global stock exchanges, had fallen significantly amid the market turmoil in FY2022. Should the capital market recover, there shall be a revaluation of investments that will leads to the creation of fair value gains in that corresponding financial year accordingly.

Audit status of RFG for the financial year ended June 30, 2021 (“FY2021”)

Background and Recap

The previous auditor of RFG accepted the resignation of MNP LLP, Chartered Professional Accountants, on April 22, 2022 as auditors of the Company. This originated from the request of MNP LLP for extending the scope of additional appropriate audit actions which included but not limited to, an onsite audit on one outstanding audit matter related to the CNY102 million deposit (the “Deposit“) placed with a PRC local fintech enterprise HuDuoBao Network Technology Co., Ltd. (“HDB“). Under COVID-19 lockdown restrictions and various limitations, RFG was unable to reach an agreement with MNP LLP on audit plan, procedure, logistical practicality and additional unfixed audit fee quotation.

RFG filed a Notice of Change of Auditor dated April 26, 2022 (the “Notice“) on SEDAR, and MNP LLP in response notified RFG that they had reviewed the Notice and they were in agreement with the statements contained in the Notice pertaining to their firm. The Notice detailed the key outstanding audit matter as follows;

“The foregoing disclosure of the business transaction with HDB forms a material part of the financial disclosure of the Company and was the subject of review, audit and verification by the Former Auditor involving physical and virtual inspections at the offices of HDB in China and as announced by the Company in its news release of April 25, 2022 such process was effectively blocked by the absolute COVID-19 lockdown restrictions in regard of the surging Omicron variant cases. China’s authorities are still accelerating efforts in mass locking down several major cities to curb the recent outbreak. Because of such difficulties, the Company and the Former Auditor could not devise a plan to complete within a reasonable period the scope of the additional appropriate audit actions required by the Former Auditor, the procedures and logistics of the action and the workaround solutions for such limitations under the COVID-19 lockdown restrictions within the Company’s budget for the audit report process.”

The latest

Since then, RFG has approached and discussed with 3 shortlisted Canadian auditing firms registered under Canadian Public Accountability Board (CPAB) on the possible appointment and feasible audit plan for the FY2021 audit. The prospective auditors all recognised the importance of performing an on-site audit procedure for the Deposit held in China, while none of them are available to travel to China or able to devise a workaround solution for the audit issue. So, none of them expressed their interest in engaging with us now in light of hurdles.

We expected the situation would last for some time. To the understanding of the management, Chinese authority concerned is still not open for non-essential travels to foreigners and particularly foreign auditors to enter China and conduct any on-site audits. There were news reports that auditors from PCAOB of the US are now allowed to inspect the auditing works of Chinese companies that are applicable for those with Hong Kong based offices whose audit can be conducted in Hong Kong. Such relief is not applicable to us as our key director and HDB relating to the unresolved audit matter are all based in China.

Moreover, China is now facing a surge in COVID-19 new variant cases while experts and projections have predicted that the situation could get severe in the coming winter months. It is reported by Reuters on December 17, 2022 that “New COVID model predicts over 1 million deaths in China through 2023” makes it even harder for any foreign auditor to go onsite to conduct the audit assuming Chinese authority approval is given.

A shortlisted Canadian auditing firm informed us they would reconsider accepting our appointment when the above limitations is fully removed and/or the Deposit at HDB is returned, utilised or settled such that the on-site audit at HDB office in China is no longer a necessary audit procedure or can be superseded by alternative audit procedure.

Cease Trade Order (“CTO”) Status

In light of the current cease trade order caused by the outstanding audit matter, we are also exploring other options like corporate restructuring exercise and considering potential mergers or acquisition offers to work around the dilemma for the sake of regaining corporate and shareholders’ value, in case the Company could not resume its trading in near term. As shareholders’ interest is always our top priority, we are completely committed to doing everything we can to get over the obstacle, so as to enable our shareholders to trade their shares freely in any way and manner as soon as possible.

RFG reached out to BCSC trying to seek possible ways to lift the CTO no matter partially or temporarily, and the communication is still in process. Our justification is that it is almost impossible for a Canadian auditing firm to conduct the audit under the various authorities’ controls and limitations in China as explained above.

Since December 2021 when the Board was aware of the fact that our ex-China Director had represented RFG to make the Deposit payment to HDB, RFG has been in close communication with HDB in exploring the way to utilise the Deposit through a 3-Year “Solution As A Service” (the “SaaS“) Cloud-based System Right-to-Use Agreement. As the related Fintech business in relation to the SaaS Agreement cannot be commenced in China due to the prolonged lockdown in major cities in China, RFG is now negotiating with HDB to refund RFG the Deposit outside of China which requires Chinese State Administration of Foreign Exchange and State Taxation Administration approvals. HDB informed us they are still checking with their local legal, finance and tax experts. Up to date, HDB acknowledged to us that the balance of the Deposit remains in full.

As announced on 4 November 2022, RFP entered into share purchase agreements with Mr. Huang Chuan and Mr. Xu Zhiyang for RFP to acquire all of the outstanding share capital of Asia Oaktree Financial Pte Ltd and Raffles Financial Technology (China) Limited respectively from both parties to achieve a business collaboration. Subsequent, Mr. Huang Chuan is appointed as the Chief Executive Officer of RFG. Mr. Huang Chuan, being a China-based businessman, will attempt to work with HDB to settle the unresolved audit issue to get rid of the current CTO. Mr Xu Zhiyang is also committed to leverage his network and resource in China to facilitate the collection of the Deposit from HDB or seek a potential party or entity potential who could do a swap of the Deposit in China by overseas money.

Proposed Reorganisation

As announced earlier on October 19, 2022, considering the current cease trade order caused by the outstanding audit matter, RFG is working with our legal team on a possible reorganisation to help RFG shareholders regain value from the ceased trade shares. The assessment in legal and financial requirement on US SEC for the proposed reorganisation is still ongoing, in particular, the business structure in the US newly set up corporation and the filing requirements for issuing free shares to public shareholders under Regulation A equity crowdfunding rules.

Proposed assignment of SaaS agreement

As announced earlier on October 19, 2022, RFG is also in a discussion with a potential assignee for a proposal of assigning all the contractual rights and obligations of RFG’s SaaS Agreement as well as the right to the utilisation of the CAD20 million performance deposit placed with HDB, to his nominated financial institution, in exchange for offshore cash, assets, or any financial instrument (“Offshore Assets”) that is acceptable to RFG outside of China with a total valuation of not less than CAD 20 million, and that will be further assigned to us by an irrecoverable arrangement (the “Assignment“).

Shall the Offshore Assets be not in cash, the Swap Assignment shall include the condition precedents are as follows;

-

the financial instrument to be transferred to us shall be accessible to us for due diligence, capitalization appraisal and evaluation to be performed by RFG or third-party professionals commissioned by RFG;

-

the financial instruments shall be fully paid up and are free and clear of all security interests, pledges, mortgages, liens, charges, encumbrances, adverse claims or restrictions of any kind, including, without limitation, any restrictions on the voting or transfer thereof (collectively, “Encumbrances”).

-

A written consent is obtained from HDB for the Assignment.

RFG also intends to distribute the Offshore Assets collected by dividend in species to RFG shareholders. RFG believes the distribution will be in the best interest of the existing shareholders of RFG. The discussion is still ongoing up to date.

Proposed Offset against the Deposit

RFG is also proposing to its major Chinese shareholders in China to sell their shares back to us which can be settled by the Deposit within the China boundary. So, the Deposit can be utilised and freely transferred among entities or individuals within the China boundary. This would lead to a share buy-back by settlement against the Deposit and cancellation of shares. Whereby this offset can possibly address RFG audit outstanding matter in the FY2021 audit which was frustrated by China’s Covid-19 safety management measures resulting in the auditors’ being unable to be on-site in China to complete the audit procedure on the Deposit.

If the major Chinese shareholders are welcomed to this proposal, we will further negotiate the terms and condition of the transaction and will seek approval from the Board of Directors, shareholders and/or Commission under the Company By-laws, all applicable rules and regulations.

We believe all of our approaches as stated above is the best course of action to relieve the Company and shareholders of the impact and suffering this event has caused all of us.

We thank all stakeholders for your care and patience during this difficult time and we do whatever we can to seek relief that this event has caused us. We will keep all stakeholders duly updated.

About Raffles Financial Group Limited (CSE: RICH) (FSE: 4VO) (OTC: RAFFF) Raffles Financial Group is listed on the Canadian Securities Exchange Purchasable under the stock symbol (RICH:CN), the Frankfurt Stock Exchange Purchasable under the stock symbol (FSE: 4VO) and the OTC Markets under the stock symbol (OTC: RAFFF).

On behalf of the RFG Board of Directors

Monita Faris

Corporate Secretary

Phone: (604) 283-6110

Email: [email protected]

Website: www.RafflesFinancial.co

The CSE has not reviewed and does not accept responsibility for the accuracy or adequacy of this release.

Neither the Canadian Securities Purchase nor its Regulation Services Provider (as that term is defined in the policies of the Canadian Securities Purchase) accepts responsibility for the adequacy or accuracy of this release. Certain statements contained in this release may constitute “forward-looking statements” or “forward-looking information” (collectively “forward-looking information”) as those terms are used in Canadian securities laws. These statements relate to future events or future performance. The use of any of the words “could”, “intend”, “expect”, “believe”, “will”, “projected”, “estimated”, “anticipates” and similar expressions and statements relating to matters that are not historical facts are intended to identify forward-looking information and are based on the Company’s current belief or assumptions as to the outcome and timing of such future events.

1 The audited financial statements in the audit report of RFP are the separate financial statements of RFP prepared in accordance with International Financial Reporting Standards. RFP is exempted from preparation of consolidated financial statements as it is a wholly-owned subsidiary corporation of Raffles Financial Group Limited which produces consolidated financial statements available for public use.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/149558

Modern brands stake on influencer marketing, with 76% of users making a purchase after seeing a product on social media.The cryptocurrency industry is no exception to this trend. However, promoting crypto products through influencer marketing can be particularly challenging. Crypto influencers pose a significant risk to a brand’s reputation and ROI due to rampant scams. Approximately 80% of channels provide fake statistics, including followers counts and engagement metrics. Additionally, this niche is characterized by high CPMs, which can increase the risk of financial loss for brands.

In this article Nadia Bubennnikova, Head of agency Famesters, will explore the most important things to look for in crypto channels to find the perfect match for influencer marketing collaborations.

-

Comments

There are several levels related to this point.

LEVEL 1

Analyze approximately 10 of the channel’s latest videos, looking through the comments to ensure they are not purchased from dubious sources. For example, such comments as “Yes sir, great video!”; “Thanks!”; “Love you man!”; “Quality content”, and others most certainly are bot-generated and should be avoided.

Just to compare:

LEVEL 2

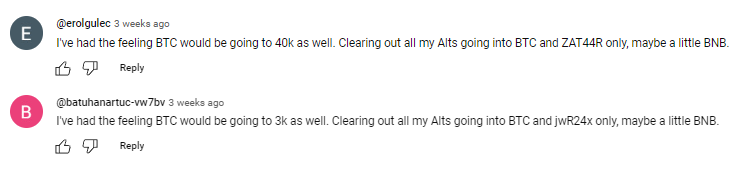

Don’t rush to conclude that you’ve discovered the perfect crypto channel just because you’ve come across some logical comments that align with the video’s topic. This may seem controversial, but it’s important to dive deeper. When you encounter a channel with logical comments, ensure that they are unique and not duplicated under the description box. Some creators are smarter than just buying comments from the first link that Google shows you when you search “buy YouTube comments”. They generate topics, provide multiple examples, or upload lists of examples, all produced by AI. You can either manually review the comments or use a script to parse all the YouTube comments into an Excel file. Then, add a formula to highlight any duplicates.

LEVEL 3

It is also a must to check the names of the profiles that leave the comments: most of the bot-generated comments are easy to track: they will all have the usernames made of random symbols and numbers, random first and last name combinations, “Habibi”, etc. No profile pictures on all comments is also a red flag.

LEVEL 4

Another important factor to consider when assessing comment authenticity is the posting date. If all the comments were posted on the same day, it’s likely that the traffic was purchased.

2. Average views number per video

This is indeed one of the key metrics to consider when selecting an influencer for collaboration, regardless of the product type. What specific factors should we focus on?

First & foremost: the views dynamics on the channel. The most desirable type of YouTube channel in terms of views is one that maintains stable viewership across all of its videos. This stability serves as proof of an active and loyal audience genuinely interested in the creator’s content, unlike channels where views vary significantly from one video to another.

Many unauthentic crypto channels not only buy YouTube comments but also invest in increasing video views to create the impression of stability. So, what exactly should we look at in terms of views? Firstly, calculate the average number of views based on the ten latest videos. Then, compare this figure to the views of the most recent videos posted within the past week. If you notice that these new videos have nearly the same number of views as those posted a month or two ago, it’s a clear red flag. Typically, a YouTube channel experiences lower views on new videos, with the number increasing organically each day as the audience engages with the content. If you see a video posted just three days ago already garnering 30k views, matching the total views of older videos, it’s a sign of fraudulent traffic purchased to create the illusion of view stability.

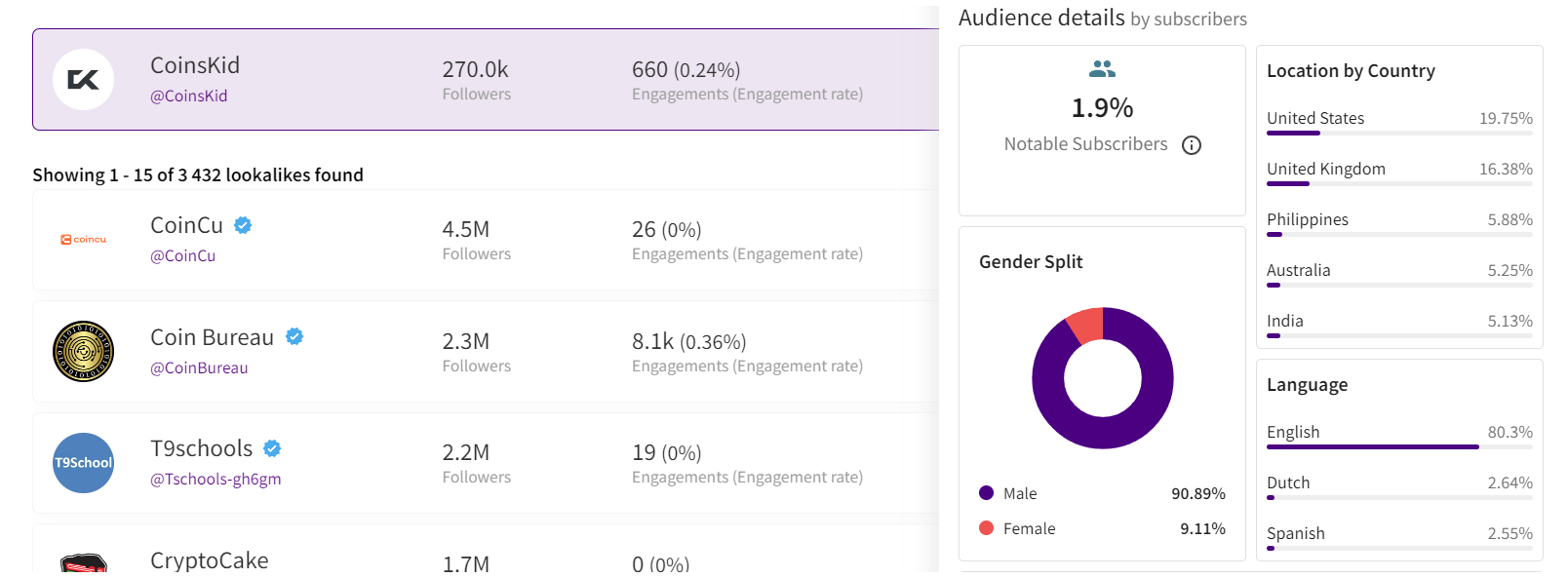

3. Influencer’s channel statistics

The primary statistics of interest are region and demographic split, and sometimes the device types of the viewers.

LEVEL 1

When reviewing the shared statistics, the first step is to request a video screencast instead of a simple screenshot. This is because it takes more time to organically edit a video than a screenshot, making it harder to manipulate the statistics. If the creator refuses, step two (if only screenshots are provided) is to download them and check the file’s properties on your computer. Look for details such as whether it was created with Adobe Photoshop or the color profile, typically Adobe RGB, to determine if the screenshot has been edited.

LEVEL 2

After confirming the authenticity of the stats screenshot, it’s crucial to analyze the data. For instance, if you’re examining a channel conducted in Spanish with all videos filmed in the same language, it would raise concerns to find a significant audience from countries like India or Turkey. This discrepancy, where the audience doesn’t align with regions known for speaking the language, is a red flag.

If we’re considering an English-language crypto channel, it typically suggests an international audience, as English’s global use for quality educational content on niche topics like crypto. However, certain considerations apply. For instance, if an English-speaking channel shows a significant percentage of Polish viewers (15% to 30%) without any mention of the Polish language, it could indicate fake followers and views. However, if the channel’s creator is Polish, occasionally posts videos in Polish alongside English, and receives Polish comments, it’s important not to rush to conclusions.

Example of statistics

Example of statistics

Wrapping up

These are the main factors to consider when selecting an influencer to promote your crypto product. Once you’ve launched the campaign, there are also some markers to show which creators did bring the authentic traffic and which used some tools to create the illusion of an active and engaged audience. While this may seem obvious, it’s still worth mentioning. After the video is posted, allow 5-7 days for it to accumulate a basic number of views, then check performance metrics such as views, clicks, click-through rate (CTR), signups, and conversion rate (CR) from clicks to signups.

If you overlooked some red flags when selecting crypto channels for your launch, you might find the following outcomes: channels with high views numbers and high CTRs, demonstrating the real interest of the audience, yet with remarkably low conversion rates. In the worst-case scenario, you might witness thousands of clicks resulting in zero to just a few signups. While this might suggest technical issues in other industries, in crypto campaigns it indicates that the creator engaged in the campaign not only bought fake views and comments but also link clicks. And this happens more often than you may realize.

Summing up, choosing the right crypto creator to promote your product is indeed a tricky job that requires a lot of resources to be put into the search process.

Author

Nadia Bubennikova, Head of agency at Famesters

The BIS, along with seven leading central banks and a cohort of private financial firms, has embarked on an ambitious venture known as Project Agorá.

Named after the Greek word for “marketplace,” this initiative stands at the forefront of exploring the potential of tokenisation to significantly enhance the operational efficiency of the monetary system worldwide.

Central to this pioneering project are the Bank of France (on behalf of the Eurosystem), the Bank of Japan, the Bank of Korea, the Bank of Mexico, the Swiss National Bank, the Bank of England, and the Federal Reserve Bank of New York. These institutions have joined forces under the banner of Project Agorá, in partnership with an extensive assembly of private financial entities convened by the Institute of International Finance (IIF).

At the heart of Project Agorá is the pursuit of integrating tokenised commercial bank deposits with tokenised wholesale central bank money within a unified, public-private programmable financial platform. By harnessing the advanced capabilities of smart contracts and programmability, the project aspires to unlock new transactional possibilities that were previously infeasible or impractical, thereby fostering novel opportunities that could benefit businesses and consumers alike.

The collaborative effort seeks to address and surmount a variety of structural inefficiencies that currently plague cross-border payments. These challenges include disparate legal, regulatory, and technical standards; varying operating hours and time zones; and the heightened complexity associated with conducting financial integrity checks (such as anti-money laundering and customer verification procedures), which are often redundantly executed across multiple stages of a single transaction due to the involvement of several intermediaries.

As a beacon of experimental and exploratory projects, the BIS Innovation Hub is committed to delivering public goods to the global central banking community through initiatives like Project Agorá. In line with this mission, the BIS will soon issue a call for expressions of interest from private financial institutions eager to contribute to this ground-breaking project. The IIF will facilitate the involvement of private sector participants, extending an invitation to regulated financial institutions representing each of the seven aforementioned currencies to partake in this transformative endeavour.

Source: fintech.globa

The post Central banks and the FinTech sector unite to change global payments space appeared first on HIPTHER Alerts.

TD Bank has inked a multi-year deal with Google Cloud as it looks to streamline the development and deployment of new products and services.

The deal will see the Canadian banking group integrate the vendor’s cloud services into a wider portion of its technology solutions portfolio, a move which TD expects will enable it “to respond quickly to changing customer expectations by rolling out new features, updates, or entirely new financial products at an accelerated pace”.

This marks an expansion of the already established relationship between TD Bank and Google Cloud after the group previously adopted the vendor’s Google Kubernetes Engine (GKE) for TD Securities Automated Trading (TDSAT), the Chicago-based subsidiary of its investment banking unit, TD Securities.

TDSAT uses GKE for process automation and quantitative modelling across fixed income markets, resulting in the development of a “data-driven research platform” capable of processing large research workloads in trading.

Dan Bosman, SVP and CIO of TD Securities, claims the infrastructure has so far supported TDSAT with “compute-intensive quantitative analysis” while expanding the subsidiary’s “trading volumes and portfolio size”.

TD’s new partnership with Google Cloud will see the group attempt to replicate the same level of success across its entire portfolio.

Source: fintechfutures.com

The post TD Bank inks multi-year strategic partnership with Google Cloud appeared first on HIPTHER Alerts.

-

Fintech6 days ago

Fintech6 days agoHow to identify authenticity in crypto influencer channels

-

Latest News6 days ago

HSBC-backed fintech Monese is considering splitting its operations as it grapples with increasing losses.

-

Latest News6 days ago

EverBank has announced a groundbreaking partnership with Finzly, poised to revolutionize payment processing.

-

Latest News5 days ago

FinTech leaders express caution regarding the promises made in #Budget2024 concerning open banking, stating that the “devil is in the details.”

-

Latest News5 days ago

Gotion High-tech’s operating profit up 391% in 2023, nearly RMB 2.8 billion invested in R&D for the year

-

Latest News5 days ago

Aurionpro Solutions acquires Arya.ai, to power next generation Enterprise AI platforms for Financial Institutions

-

Latest News6 days ago

Wells Fargo, a leading financial institution, is set to revolutionize its trade finance operations by incorporating artificial intelligence (AI) technology through its collaboration with TradeSun.

-

Latest News5 days ago

Latvian Fintech inGain Raises €650,000 for No-Code SaaS Loan Management System