Fintech PR

North American Banks Risk Losing $88 Billion in Payments Revenue by 2025, According to Accenture Report

As much as 15% of North American banks’ payments revenue — $88 billion — is likely to be displaced by the growth of digital payments and competition from non-banks, as payments become more instant, invisible and free, according to a new report from Accenture (NYSE: ACN). Of the $88 billion, approximately $82 billion is attributable to U.S. banks and $6 billion to Canadian banks.

Titled “5 Big Bets in Retail Payments in North America,” the report is based on a revenue-risk analysis model that Accenture developed to measure trends in how consumers pay and projected changes in merchant behavior, technology and regulation. The research is complemented by a survey of payments executives at the 50 largest U.S. and Canadian banks by revenue to determine how they plan to mitigate and capitalize on the disruption in payments to grow customer loyalty, revenues and profitability.

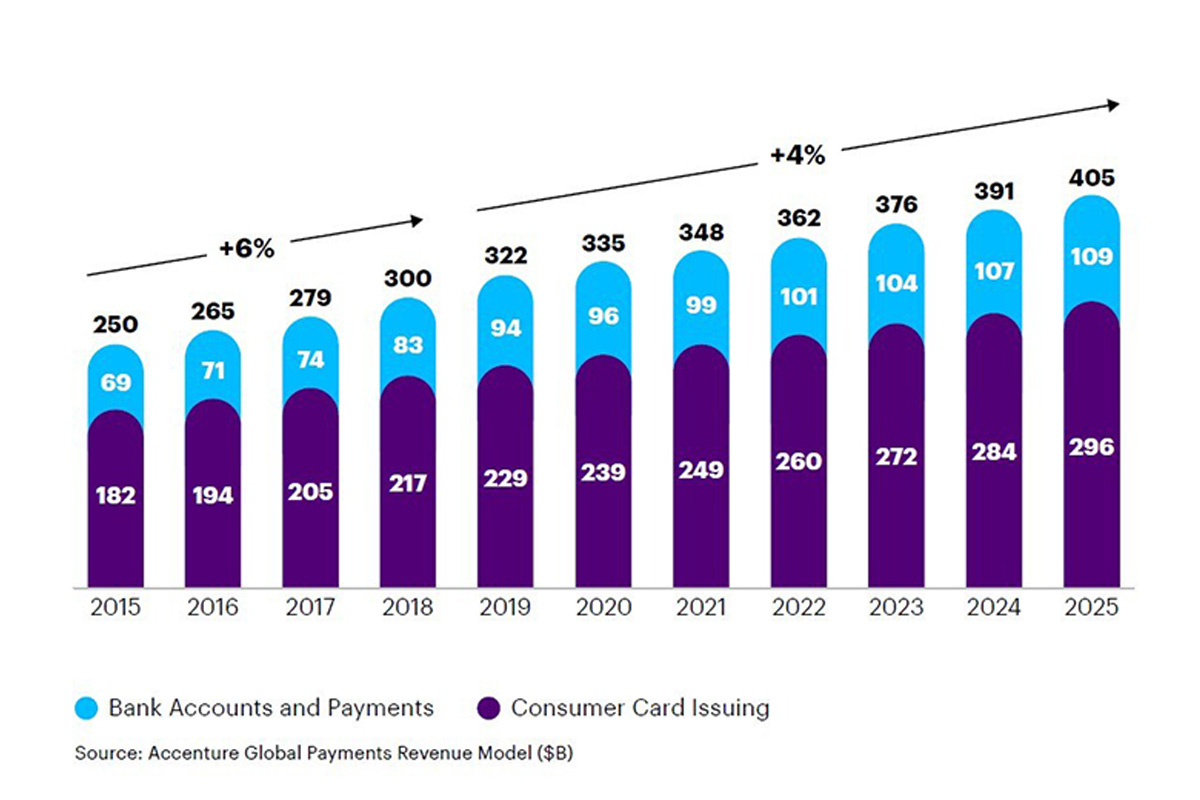

The report found that while payments revenue among North American banks is slowing, it will likely grow at a compound annual rate of 4% over the next half-dozen years — from $322 billion in 2019 to $405 billion in 2025 for retail payments (see Figure 1), and from $505 billion in 2019 to $653 billion in 2025 for retail and commercial payments combined. Only banks that change their business models to adopt the latest technologies and transform the customer experience will capture a share of the nearly $150 billion in incremental revenue growth, according to the report.

“As retail payments facilitation become increasingly commoditized, customer experience is the new driver of brand value and competitiveness,” said Andrew McFarlane, Managing Director – Payments and Global Open Banking, at Accenture in Canada. “With new entrants introducing instant and invisible payment options, combined with pricing compression, banks that are unable to shift to new business models and continually innovate face a future of revenue loss and diminishing relevancy.”

The research confirmed industry awareness of the threats posed by new players in payments. Six in 10 (60%) of the banking executives surveyed believe they will lose up to 15% of payments revenue in the next three years to non-banks, fintechs and other competitors. When asked to identify the primary challenge to their business, nearly two out of five (38%) respondents cited competition from big technology companies, and one-third (34%) cited competition from fintechs. Payments fintechs in North America attracted nearly $11 billion through more than 800 deals between 2016 and 2018 alone, according to the report.

The surveyed executives also acknowledged the challenges brought on by new technologies in payments. Six in 10 (61%) said they believe that payments are becoming free; nearly three-quarters (73%) believe that most payments are already invisible or will become so over the next 12 months; and even more (78%) said that payments are either already instant or will become instant over the next 12 months.

The report notes that the impact of consumer demand for rewards has squeezed payments revenue, with spending in loyalty and rewards by the top five U.S. card issuers jumping from $11 billion in 2010 to $31 billion in 2018. Pressure on traditional revenue models, eroding fees and increased competition will force banks to invest in value-added services to drive economic performance. Bank executives cite next-generation reward schemes and embedded payments capabilities among their priorities for generating new payment revenue, according to the report.

“Payments is North America’s largest fintech segment, and while banks continue to ponder whether fintechs are friends or foes in retail payments, in most cases the answer is both,” McFarlane said. “Banks need to determine which fintechs they want to beat, buy or join. Banks that don’t collaborate with fintechs will likely fall behind in customer experience, innovation and agility.”

Hampered by legacy systems, bank executives understand that implementing digital technologies will be essential to support innovation and efficiency. One-quarter (24%) of respondents cited artificial intelligence, robotics, machine learning and innovative payments hubs as the key platform technology capabilities they need to adapt their core systems in order to shift to high-speed and continuous payment flows.

SOURCE Accenture

STOCKHOLM, April 5, 2024 /PRNewswire/ — EQT AB’s Q1 Announcement 2024 will be published on Thursday 18 April 2024 at approximately 07:30 CEST. EQT will host a conference call at 08:30 CEST to present the report, followed by a Q&A session.

The presentation and a video link for the webcast will be available here from the time of the publication of the Q1 Announcement.

To participate by phone and ask questions during the Q&A, please register here in advance. Upon registration, you will receive your personal dial-in details.

The webcast can be followed live here and a recording will be available afterwards.

Information on EQT AB’s financial reporting

The EQT AB Group has a long-term business model founded on a promise to its fund investors to invest capital, drive value creation and create consistent attractive returns over a 5 to 10-year horizon. The Group’s financial model is primarily affected by the size of its fee-generating assets under management, the performance of the EQT funds and its ability to recruit and retain top talent.

The Group operates in a market driven by long-term trends and thus believes quarterly financial statements are less relevant for investors. However, in order to provide the market with relevant and suitable information about the Group’s development, EQT publishes quarterly announcements with key operating numbers that are relevant for the business performance (taking Nasdaq’s guidance note for preparing interim management statements into consideration). In addition, a half-year report and a year-end report including financial statements and further information relevant for investors is published. Finally, EQT also publishes an annual report including sustainability reporting.

Contact

Olof Svensson, Head of Shareholder Relations, +46 72 989 09 15

EQT Shareholder Relations, [email protected]

Rickard Buch, Head of Corporate Communications, +46 72 989 09 11

EQT Press Office, [email protected], +46 8 506 55 334

This information was brought to you by Cision http://news.cision.com

https://news.cision.com/eqt/r/invitation-to-presentation-of-eqt-ab-s-q1-announcement-2024,c3956826

The following files are available for download:

|

Invitation to presentation of EQT AB’s Q1 Announcement 2024 |

|

|

EQT AB Group |

View original content:https://www.prnewswire.co.uk/news-releases/invitation-to-presentation-of-eqt-abs-q1-announcement-2024-302109147.html

- Kia drives forward transformation into ‘Sustainable Mobility Solutions Provider’

- Roadmap enables Kia to proactively respond to uncertainties in mobility industry landscape, including changes in EV market

- Company to expand EV line-up with more models; enhance HEV line-up to manage fluctuation in EV demand

- Goal to sell 1.6 million EVs annually in 2030, introducing 15 models

- PBV to play a key role in Kia’s growth, targeting 250,000 PBV sales annually by 2030 with PV5 and PV7 models

- Kia to invest KRW 38 trillion by 2028, including KRW 15 trillion for future business

- 2024 business guidance : KRW 101 tln in revenue with KRW 12 tln in operating profit; operating profit margin of 11.9% on sales of 3.2 million units globally

- CEO reaffirms Kia’s commitment to ESG management

SEOUL, South Korea, April 5, 2024 /PRNewswire/ — Kia Corporation (Kia) today shared an update on its future strategies and financial targets at its CEO Investor Day in Seoul, Korea.

Based on its innovative achievements in the years since the announcement of mid-to-long-term business initiatives, Kia is focusing on updating its 2030 strategy announced last year and further strengthening its business strategy in response to uncertainties across the global mobility industry landscape.

During the event, Kia updated its mid-to-long-term business strategy with a focus on electrification, and its PBV business. Kia reiterated its 2030 annual sales target of 4.3 million units, including 1.6 million units of electric vehicles (EVs). The 2030 4.3 million annual sales target is 34.4 percent higher than the brand’s 2024 annual goal of 3.2 million units.

The company also plans to become a leading EV brand by selling a higher percentage of electrified models among its total sales, including hybrid electric vehicles (HEV), plug-in hybrid (PHEV), and battery EVs, projecting electrified model sales of 2.48 million units annually or 58 percent of Kia’s total sales in 2030.

“Following our successful brand relaunch in 2021, Kia is enhancing its global business strategy to further the establishment of an innovative EV line-up and accelerate the company’s transition to a sustainable mobility solutions provider,” said Ho Sung Song, President and CEO of Kia. “By responding effectively to changes in the mobility market and efficiently implementing mid-to-long-term strategies, Kia is strengthening its brand commitment to the wellbeing of customers, communities, the global society, and the environment.”

Photo – https://mma.prnewswire.com/media/2380039/Photo_1__2024_CEO_Investor_Day.jpg

PDF – https://mma.prnewswire.com/media/2380040/Press_Release__2024_Kia_CEO_Investor_Day_240405.pdf

![]() View original content to download multimedia:https://www.prnewswire.co.uk/news-releases/kia-presents-roadmap-to-lead-global-electrification-era-through-evs-hevs-and-pbvs-302109142.html

View original content to download multimedia:https://www.prnewswire.co.uk/news-releases/kia-presents-roadmap-to-lead-global-electrification-era-through-evs-hevs-and-pbvs-302109142.html

VANCOUVER, BC, April 4, 2024 /PRNewswire/ — BioVaxys Technology Corp. (CSE: BIOV) (FRA: 5LB) (OTCQB: BVAXF) (the “Company“) is providing this bi-weekly update on the status of the management cease trade order granted on February 29, 2024 (the “MCTO“), by its principal regulator, the Ontario Securities Commission (the “OSC“), under National Policy 12-203 – Management Cease Trade Orders (“NP 12-203“), following the Company’s announcement on February 21, 2024 (the “Default Announcement“), that it was unable to file its audited annual financial statements for the year ended October 31, 2023, its management’s discussion and analysis of financial statements for the year ended October 31, 2023, its annual information form for the year ended October 31, 2023, and related filings (collectively, the “Required Annual Filings“). Under National Instrument 51-102, the Required Annual Filings were required to be made no later than February 28, 2024.

As a result of the delay in filing the Required Annual Filings, the Company was unable to file its interim financial statements for the three months ended January 31, 2024, its management’s discussion and analysis of financial statements for the three months ended January 31, 2024, and related filings (collectively, the “Required Interim Filings“). Under National Instrument 51-102, the Required Interim Filings were required to be made no later than April 1, 2024.

The Company anticipates filing the Required Annual Filings by April 30, 2024. The auditor of the Company requires additional time to complete its audit of the Company, including the Company’s recent acquisition of all intellectual property, immunotherapeutics platform technologies, and clinical stage assets of the former IMV Inc. that closed on February 16, 2024. In addition, the Company anticipates filing the Required Interim Filings immediately after the filing of the Required Annual Filings.

Except as herein disclosed, there are no material changes to the information contained in the Default Announcement. In addition, (i) the Company is satisfying and confirms that it intends to continue to satisfy the provisions of the alternative information guidelines under NP 12-203 and issue bi-weekly default status reports for so long as the delay in filing the Required Annual Filings and/or Required Interim Filings is continuing, each of which will be issued in the form of a press release; (ii) the Company does not have any information at this time regarding any anticipated specified default subsequent to the default in filing the Required Annual Filings and Required Interim Filings; (iii) the Company is not subject to any insolvency proceedings; and (iv) there is no material information concerning the affairs of the Company that has not been generally disclosed.

About BioVaxys Technology Corp.

BioVaxys Technology Corp. (www.biovaxys.com), a biopharmaceuticals company registered in British Columbia, Canada, is a clinical-stage biopharmaceutical company dedicated to improving patient lives with novel immunotherapies based on the DPX™ immune-educating technology platform and it’s HapTenix© ‘neoantigen’ tumor cell construct platform, for treating cancers, infectious disease, antigen desensitization, and other immunological fields. The Company’s clinical stage pipeline includes maveropepimut-S which is in Phase II clinical development for advanced Relapsed-Refractory Diffuse Large B Cell Lymphoma (DLBCL) and platinum resistant ovarian cancer, and BVX-0918, a personalized immunotherapeutic vaccine using it proprietary HapTenix© ‘neoantigen’ tumor cell construct platform which is soon to enter Phase I in Spain for treating refractive late-stage ovarian cancer. The Company is also capitalizing on its tumor immunology know-how and creation of a unique library of T-lymphocytes & other datasets post-vaccination with its personalized immunotherapeutic vaccines to utilize predictive algorithms and other technologies to identify new targetable tumor antigens. BioVaxys common shares are listed on the CSE under the stock symbol “BIOV” and trade on the Frankfurt Bourse (FRA: 5LB) and in the US (OTCQB: BVAXF). For more information, visit www.biovaxys.com and connect with us on X and LinkedIn.

ON BEHALF OF THE BOARD

Signed “James Passin“

James Passin, Chief Executive Officer

Phone: +1 646 452 7054

Logo – https://mma.prnewswire.com/media/1430981/BIOVAXYS_Logo.jpg

![]() View original content:https://www.prnewswire.co.uk/news-releases/biovaxys-technology-corp-provides-bi-weekly-mcto-status-update-302108920.html

View original content:https://www.prnewswire.co.uk/news-releases/biovaxys-technology-corp-provides-bi-weekly-mcto-status-update-302108920.html

-

Latest News7 days ago

HSBC-backed fintech Monese is considering splitting its operations as it grapples with increasing losses.

-

Latest News7 days ago

EverBank has announced a groundbreaking partnership with Finzly, poised to revolutionize payment processing.

-

Latest News6 days ago

FinTech leaders express caution regarding the promises made in #Budget2024 concerning open banking, stating that the “devil is in the details.”

-

Latest News6 days ago

Aurionpro Solutions acquires Arya.ai, to power next generation Enterprise AI platforms for Financial Institutions

-

Latest News6 days ago

Gotion High-tech’s operating profit up 391% in 2023, nearly RMB 2.8 billion invested in R&D for the year

-

Latest News7 days ago

Wells Fargo, a leading financial institution, is set to revolutionize its trade finance operations by incorporating artificial intelligence (AI) technology through its collaboration with TradeSun.

-

Latest News6 days ago

Latvian Fintech inGain Raises €650,000 for No-Code SaaS Loan Management System

-

Latest News6 days ago

Credit card fintech Pliant lands €18m Series A extension led by PayPal Ventures