Fintech

Magen and Grey Wolf Enter into Business Combination Agreement to Complete Qualifying Transaction

Toronto, Ontario–(Newsfile Corp. – March 17, 2022) – Magen Ventures I Inc. (TSXV: MAGN.P) (“Magen“) and Grey Wolf Animal Health Inc. (“Grey Wolf“) are pleased to announce that, further to Magen’s news release of January 26, 2022, they have entered into a business combination agreement dated March 16, 2022 (the “BCA“), which outlines the terms and conditions pursuant to which Magen and Grey Wolf will complete a transaction that will result in a reverse take-over of Magen by Grey Wolf (the “Proposed Transaction“). The Proposed Transaction will be an arm’s length transaction, and, if completed, will constitute Magen’s “Qualifying Transaction” (as such term is defined in Policy 2.4 of the TSX Venture Exchange (the “TSXV“)). Magen following the completion of the Proposed Transaction is referred to as the “Resulting Issuer“.

Grey Wolf Animal Health Inc.

Grey Wolf is a diversified animal health company founded by Dr. Ian Sandler, an entrepreneurial veterinarian, and led by an experienced pharmaceutical management team. Grey Wolf is a corporation existing under the Business Corporations Act (Ontario) and was amalgamated on December 31, 2020.

Grey Wolf is focused on bringing to market a broad portfolio of products that meet the unmet needs of veterinarians, clinics and pet parents across Canada. In the past three years, Grey Wolf has launched five new product portfolios and has augmented its strong organic revenue growth with two strategic acquisitions.

The animal health sector has historically been recession-resistant and has grown at a compound annual growth rate (CAGR) of 6.5% over the past 15 years.[1] Industry growth has accelerated in recent years as pets are increasingly viewed as members of the family with millennials choosing pets over children and surpassing baby-boomers as the largest demographic buying group. This increased ‘humanization’ of pets leads to increased spend both on health and wellness as well as therapeutics and other treatments.[2]

Grey Wolf markets products in the veterinary channel for use in companion animals (primarily dogs and cats) and equine. Grey Wolf’s revenue is derived primarily from three main product areas:

- Pharmaceuticals – including species-specific, human off-label and custom formulated prescription products.

- Nutraceuticals – low risk veterinary health products, including a novel, non-antibiotic product basket for treating gastro-intestinal upset, the number one cause of non-routine vet visits.

- Consumables – including medical pet-shirts that replace the ‘cone of shame’ and an innovative, all-natural wound-care line that uses manuka honey in lieu of traditional antibiotic solutions.

On September 1, 2021, Grey Wolf completed the acquisition of Trutina Pharmacy Inc. (“Trutina“), a highly profitable compounding pharmacy focused on the equine market. Proforma the acquisition of Trutina as at December 31, 2021, management of Grey Wolf expects Grey Wolf to have approximately $20 million in annualized revenue and positive free cash flow.

The following table contains selected financial information in respect of Grey Wolf as at December 31, 2021, which includes four months of Trutina’s results.

| Year ended December 31, 2021 (unaudited) |

|

| Assets | $33,027,126 |

| Liabilities | $31,217,367 |

| Revenues | $13,095,439 |

| Net Profit (Losses) | ($720,375) |

As at December 31, 2021, Grey Wolf had $4.3 million in cash, a 5-year, low-interest rate term loan with Canadian Western Bank for $11.3 million and an undrawn line of credit. When combined with Magen’s cash ($4.5 million as at September 30, 2021) and Grey Wolf’s existing cash flow, Grey Wolf will have a strong balance sheet to pursue its organic growth initiatives and potential strategic acquisitions. As a result, Grey Wolf does not intend to pursue a concurrent financing as part of the Proposed Transaction.

The audit of Grey Wolf’s financial statements for the year ended December 31, 2021 is not yet complete and the above financial information is therefore subject to change.

Magen Ventures I Inc.

Magen was incorporated under the Business Corporations Act (Ontario) on February 9, 2021 and is a Capital Pool Company (as defined in the policies of the TSXV) listed on the TSXV. Magen has no commercial operations and no assets other than cash.

Consolidation

Prior to the closing of the Proposed Transaction, to align the value of the Magen common shares (the “Magen Shares“) with the value per Grey Wolf Common Share (as defined below) at which the Proposed Transaction will be completed, it is anticipated that Magen will consolidate the Magen Shares on the basis of the Consolidation Ratio (as defined below) (the “Consolidation“). The “Consolidation Ratio” is equal to 1 post-Consolidation Magen Share for every 19.1667 pre-Consolidation Magen Share, or such other ratio mutually agreed between the parties. Assuming the above Consolidation Ratio, the Consolidation will result in an aggregate of approximately 3,130,429 post-Consolidation Magen Shares being outstanding based on there being 60,000,000 Magen Shares currently outstanding (and assuming no intervening exercise of options or warrants). The Consolidation will also result in an adjustment to the number of post-Consolidation Magen Shares issuable pursuant to outstanding options (of which there are now 6,000,000 outstanding) and warrants (of which there are now 3,200,000 outstanding), from a pre-Consolidation total of 9,200,000 Magen Shares issuable upon exercise thereof to a post-Consolidation total of (assuming the above Consolidation Ratio) approximately 479,999 Magen Shares issuable upon exercise.

Proposed Transaction Summary

The Proposed Transaction is structured as a three-cornered amalgamation, whereby a wholly-owned subsidiary of Magen formed for such purpose will amalgamate with Grey Wolf (the “Amalgamation“) to form a newly amalgamated company (“Amalco“). In consideration for the Proposed Transaction, holders of common shares of Grey Wolf (“Grey Wolf Common Shares“) and other securities of Grey Wolf will receive corresponding securities of the Resulting Issuer pursuant to the Amalgamation.

Upon completion of the Proposed Transaction, the Resulting Issuer will be the parent and sole shareholder of Amalco and thus will indirectly carry on the business of Grey Wolf. The current shareholders of Grey Wolf will become shareholders of the Resulting Issuer, as the new parent corporation, and the Magen shareholders will retain their equity in the Resulting Issuer. It is expected that approximately 25,900,000 post-Consolidation Magen Shares (“Resulting Issuer Shares“) will be issued to the shareholders of Grey Wolf at a deemed price of $2.30 per Resulting Issuer Share. As a result, the Resulting Issuer is expected to have approximately 29,000,000 Resulting Issuer Shares outstanding immediately following the completion of the Proposed Transaction. Outstanding options and warrants of Grey Wolf will also be exchanged pursuant to the Amalgamation for replacement options and warrants of the Resulting Issuer (on substantially the same economic terms), which will be exercisable for an aggregate of 4,296,300 Resulting Issuer Shares.

In connection with the Proposed Transaction, the Resulting Issuer intends to change its name to “Grey Wolf Animal Health Corp.” or such other name as is acceptable to the regulators (the “Name Change“). Further, it is proposed that the officers and directors of Grey Wolf will replace the existing officers and directors of Magen. Biographical information regarding these individuals is provided below under the heading “Officers and Directors“.

Completion of the Proposed Transaction is subject to a number of other conditions, including obtaining all necessary board, shareholder and regulatory approvals, including TSXV approval.

Although the Proposed Transaction itself is not subject to approval by the shareholders of Magen under applicable TSXV policies or otherwise, in connection with the Proposed Transaction, Magen will convene a meeting of its shareholders for the purpose of approving, among other matters, the Consolidation, the Name Change and the election of the directors to replace the current directors of Magen immediately following the completion of the Proposed Transaction. Grey Wolf will convene a meeting of its shareholders for the purpose of approving the Amalgamation. The Proposed Transaction has been unanimously approved by the boards of directors of Grey Wolf and Magen and both boards of directors recommend that their respective shareholders vote in favor of the Proposed Transaction and related matters.

No finder’s fee or commission is payable in relation to the Proposed Transaction.

Officers and Directors

Subject to applicable shareholder and TSXV approval, it is anticipated that the officers and directors of the Resulting Issuer will be:

Angela Cechetto – Chief Executive Officer

Angela Cechetto is the Chief Executive Officer of Grey Wolf. Ms. Cechetto joined Grey Wolf in April 2017 as Vice President of Business & Corporate Development and was appointed President in May 2018. Ms. Cechetto has more than 15 years of experience in the pharmaceutical industry in Canada and in emerging markets such as South Africa and Latin America. Prior to Grey Wolf, Ms. Cechetto was an equity research associate at GMP Securities LP, where she covered Canadian companies in the specialty pharmaceutical, medical device, and cannabis industries. Prior to GMP, Ms. Cechetto held progressive roles on the business development team at Paladin Labs Inc. from 2008-2015 culminating as Director of Business Development. Ms. Cechetto holds a B.Sc. from McGill University, a M.Sc.E.E. from the University of New Brunswick and an MBA from the Ivey Business School.

Kevin Palmer – Chief Financial Officer

Kevin Palmer is the Chief Financial Officer of Grey Wolf. Mr. Palmer joined Grey Wolf in October 2020 as Vice President of Finance. He has more than 25 years of Canadian, United States and international experience and has spent the past 20 years working in pharmaceuticals, biotech, and medical device organizations such as Sprout Pharmaceuticals, St. Jude Medical and InterMune. Mr. Palmer has led teams in finance, operations, customer service, and human resources in several companies with success in business planning and analysis, effective financial control, strategic focus, system integrations and conversions, statutory and management reporting, treasury, and tax. A graduate of UofT’s B.Comm. program, Mr. Palmer is a CPA, CA, and recently completed his MBA. Mr. Palmer volunteers with the CPA Canada’s Financial Literacy program, has taught finance courses at the undergraduate and continuing education level, and is on the Board of Directors of two not-for-profit organizations.

Dr. Ian Sandler – Chief Veterinary Medical Officer and Director

Dr. Ian Sandler is the co-Founder of Grey Wolf. Dr. Sandler graduated from University of Guelph with a Doctor of Veterinary Medicine (DVM) in 1994 and began practicing small animal medicine in the United States. He returned to Canada and in 1999, along with three colleagues, founded the Ontario Veterinary Group, which grew to be one of the largest privately-owned veterinary hospital groups in Canada. In 2014, Associate Veterinary Clinics Ltd. acquired the Ontario Veterinary Group. Dr. Sandler is a well-respected animal health expert and is frequently quoted and interviewed. He served on the Animal Health Technologist / Veterinary Technician Accreditation Committee of the Canadian Veterinary Medical Association (“CVMA“) from 2009 to 2016 and now sits on the National Issues Committee of the CVMA. Dr. Sandler has practiced small animal medicine and surgery at the Rosedale Animal Hospital for over 25 years.

Shawn Aspden – Director

Shawn Aspden serves as the Chair of the Board of Directors of Grey Wolf. Mr. Aspden is a Principal at Bloom Burton & Co., a Toronto-based investment firm focused on companies operating in the healthcare sector. Mr. Aspden has worked alongside healthcare companies for over 25 years in an institutional sales capacity and has extensive experience in raising capital for both growth and established companies. Prior to joining Bloom Burton in 2016, Mr. Aspden served as Vice Chair, Head of North American Institutional Equity Sales at GMP Securities LP, where he was a member of the firm’s Executive Committee and managed a top-ranked institutional sales team. Mr. Aspden began his career at a strategy consulting firm and moved into the investment business as an equity research associate. Mr. Aspden holds the Chartered Financial Analyst designation and is an HBA graduate from the Ivey Business School.

Rob Harris – Director

Mr. Harris has been a director of Grey Wolf since 2016 and is also the Chair of the board at Miravo Healthcare Inc., a Canadian focused healthcare company with global reach and a diversified portfolio of commercial products. Mr. Harris was previously the co-founder, director and Chief Executive Officer of Tribute Pharmaceuticals Inc., a TSX-listed Canadian specialty pharmaceutical company acquired by Pozen in 2016. Prior to co-founding Tribute Pharmaceuticals, Mr. Harris was the President & Chief Executive Officer of Legacy Pharmaceuticals Inc. Mr. Harris also has previous experience at Biovail Corporation where as Vice President of Business Development, he was involved, led and successfully concluded numerous business development transactions, including the licensing of new chemical entities, the acquisition of mature products, the completion of co-promotion deals, distribution agreements, product development and reformulation transactions. Prior to Biovail, Mr. Harris worked in various senior commercial management positions during his 20-year tenure at Wyeth (Ayerst), including its animal health group, and has been involved in numerous product launches during his career.

It is also anticipated that two additional independent directors will join the board of the Resulting Issuer.

Sponsorship

The Proposed Transaction is subject to the sponsorship requirements of the TSXV, unless a waiver or exemption from this requirement can be obtained in accordance with the policies of the TSXV. Magen intends to apply for a waiver of the sponsorship requirement, however there is no assurance that a waiver from this requirement can or will be obtained.

Trading in Magen Shares

Trading in Magen Shares has been halted in compliance with the policies of the TSXV. Trading in the Magen Shares will remain halted pending the review of the Proposed Transaction by the TSXV and satisfaction of the conditions of the TSXV for resumption of trading. It is likely that trading in the Magen Shares will not resume prior to the closing of the Proposed Transaction.

Non-Arm’s Length Party Interest

The spouse of Jesse Kaplan, an officer and director of Magen, is the holder of certain convertible debt securities of Grey Wolf.

Grey Wolf is represented by DLA Piper (Canada) LLP. Dentons Canada LLP acts as legal counsel to Magen.

This news release does not constitute an offer of securities for sale in the United States. The securities being offered have not been, nor will they be, registered under the United States Securities Act of 1933, as amended, and such securities may not be offered or sold within the United States absent U.S. registration or an applicable exemption from U.S. registration requirements.

All information provided in this press release relating to Grey Wolf and the proposed officers and directors has been provided by management of Grey Wolf and has not been independently verified by management of Magen.

Cautionary Note Regarding Forward-Looking Information

This press release contains statements which constitute “forward-looking information” within the meaning of applicable securities laws, including statements regarding the plans, intentions, beliefs and current expectations of Magen and Grey Wolf with respect to future business activities and operating performance. Forward-looking information is often identified by the words “may”, “would”, “could”, “should”, “will”, “intend”, “plan”, “anticipate”, “believe”, “estimate”, “expect” or similar expressions and includes information regarding: (i) expectations regarding whether the Proposed Transaction will be consummated, including whether conditions to the consummation of the Proposed Transaction will be satisfied, or the timing for completing the Proposed Transaction, (ii) future annualized revenue, (iii) proposed directors and officers of the Resulting Issuer, (iv) the expected number of Resulting Issuer Shares upon completion of the Proposed Transaction, and (v) expectations for other economic, business, and/or competitive factors.

Investors are cautioned that forward-looking information is not based on historical facts but instead reflect Magen and Grey Wolf’s respective management’s expectations, estimates or projections concerning future results or events based on the opinions, assumptions and estimates of management considered reasonable at the date the statements are made. Although Magen and Grey Wolf believe that the expectations reflected in such forward-looking information are reasonable, such information involves risks and uncertainties, and undue reliance should not be placed on such information, as unknown or unpredictable factors could have material adverse effects on future results, performance or achievements of the Resulting Issuers. Among the key factors that could cause actual results to differ materially from those projected in the forward-looking information are the following: the ability to consummate the Proposed Transaction; the ability to obtain requisite regulatory and shareholder approvals and the satisfaction of other conditions to the consummation of the Proposed Transaction on the proposed terms and schedule; the potential impact of the announcement or consummation of the Proposed Transaction on relationships, including with regulatory bodies, employees, suppliers, customers and competitors; changes in general economic, business and political conditions, including changes in the financial markets; changes in applicable laws; and the diversion of management time on the Proposed Transaction. This forward-looking information may be affected by risks and uncertainties in the business of Magen and Grey Wolf and market conditions.

Should one or more of these risks or uncertainties materialize, or should assumptions underlying the forward-looking information prove incorrect, actual results may vary materially from those described herein as intended, planned, anticipated, believed, estimated or expected. Although Magen and Grey Wolf have attempted to identify important risks, uncertainties and factors which could cause actual results to differ materially, there may be others that cause results not to be as anticipated, estimated or intended. Magen and Grey Wolf do not intend, and do not assume any obligation, to update this forward-looking information except as otherwise required by applicable law.

For further information, please contact:

Grey Wolf Animal Health Inc.

Angela Cechetto

Chief Executive Officer

E-mail: [email protected]

Magen Ventures I Inc.

Jesse Kaplan

Chief Executive Officer

E-mail: [email protected]

Completion of the Proposed Transaction is subject to a number of conditions, including but not limited to TSXV acceptance and, if applicable pursuant to TSXV requirements, majority of the minority shareholder approval. Where applicable, the Proposed Transaction cannot close until the required shareholder approval is obtained. There can be no assurance that the Proposed Transaction will be completed as proposed or at all.

Investors are cautioned that, except as disclosed in the filing statement to be prepared in connection with the Proposed Transaction, any information released or received with respect to the Proposed Transaction may not be accurate or complete and should not be relied upon. Trading in the securities of Magen should be considered highly speculative.

The TSXV has in no way passed upon the merits of the Proposed Transaction and has not approved or disapproved of the contents of this news release.

Neither the TSXV nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this release.

[1] Adapted from: Statistics Canada. Tables 36-10-0124-01 and 36-10-0225-01

[2] American Pet Products Association

NOT FOR DISTRIBUTION TO UNITED STATES NEWSWIRE SERVICES OR FOR

DISSEMINATION IN THE UNITED STATES

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/117148

Modern brands stake on influencer marketing, with 76% of users making a purchase after seeing a product on social media.The cryptocurrency industry is no exception to this trend. However, promoting crypto products through influencer marketing can be particularly challenging. Crypto influencers pose a significant risk to a brand’s reputation and ROI due to rampant scams. Approximately 80% of channels provide fake statistics, including followers counts and engagement metrics. Additionally, this niche is characterized by high CPMs, which can increase the risk of financial loss for brands.

In this article Nadia Bubennnikova, Head of agency Famesters, will explore the most important things to look for in crypto channels to find the perfect match for influencer marketing collaborations.

-

Comments

There are several levels related to this point.

LEVEL 1

Analyze approximately 10 of the channel’s latest videos, looking through the comments to ensure they are not purchased from dubious sources. For example, such comments as “Yes sir, great video!”; “Thanks!”; “Love you man!”; “Quality content”, and others most certainly are bot-generated and should be avoided.

Just to compare:

LEVEL 2

Don’t rush to conclude that you’ve discovered the perfect crypto channel just because you’ve come across some logical comments that align with the video’s topic. This may seem controversial, but it’s important to dive deeper. When you encounter a channel with logical comments, ensure that they are unique and not duplicated under the description box. Some creators are smarter than just buying comments from the first link that Google shows you when you search “buy YouTube comments”. They generate topics, provide multiple examples, or upload lists of examples, all produced by AI. You can either manually review the comments or use a script to parse all the YouTube comments into an Excel file. Then, add a formula to highlight any duplicates.

LEVEL 3

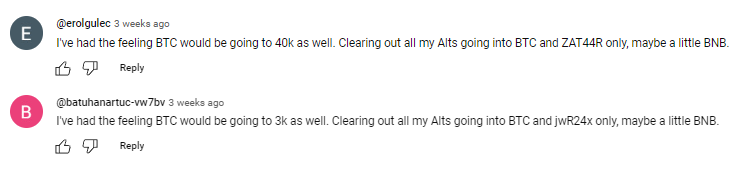

It is also a must to check the names of the profiles that leave the comments: most of the bot-generated comments are easy to track: they will all have the usernames made of random symbols and numbers, random first and last name combinations, “Habibi”, etc. No profile pictures on all comments is also a red flag.

LEVEL 4

Another important factor to consider when assessing comment authenticity is the posting date. If all the comments were posted on the same day, it’s likely that the traffic was purchased.

2. Average views number per video

This is indeed one of the key metrics to consider when selecting an influencer for collaboration, regardless of the product type. What specific factors should we focus on?

First & foremost: the views dynamics on the channel. The most desirable type of YouTube channel in terms of views is one that maintains stable viewership across all of its videos. This stability serves as proof of an active and loyal audience genuinely interested in the creator’s content, unlike channels where views vary significantly from one video to another.

Many unauthentic crypto channels not only buy YouTube comments but also invest in increasing video views to create the impression of stability. So, what exactly should we look at in terms of views? Firstly, calculate the average number of views based on the ten latest videos. Then, compare this figure to the views of the most recent videos posted within the past week. If you notice that these new videos have nearly the same number of views as those posted a month or two ago, it’s a clear red flag. Typically, a YouTube channel experiences lower views on new videos, with the number increasing organically each day as the audience engages with the content. If you see a video posted just three days ago already garnering 30k views, matching the total views of older videos, it’s a sign of fraudulent traffic purchased to create the illusion of view stability.

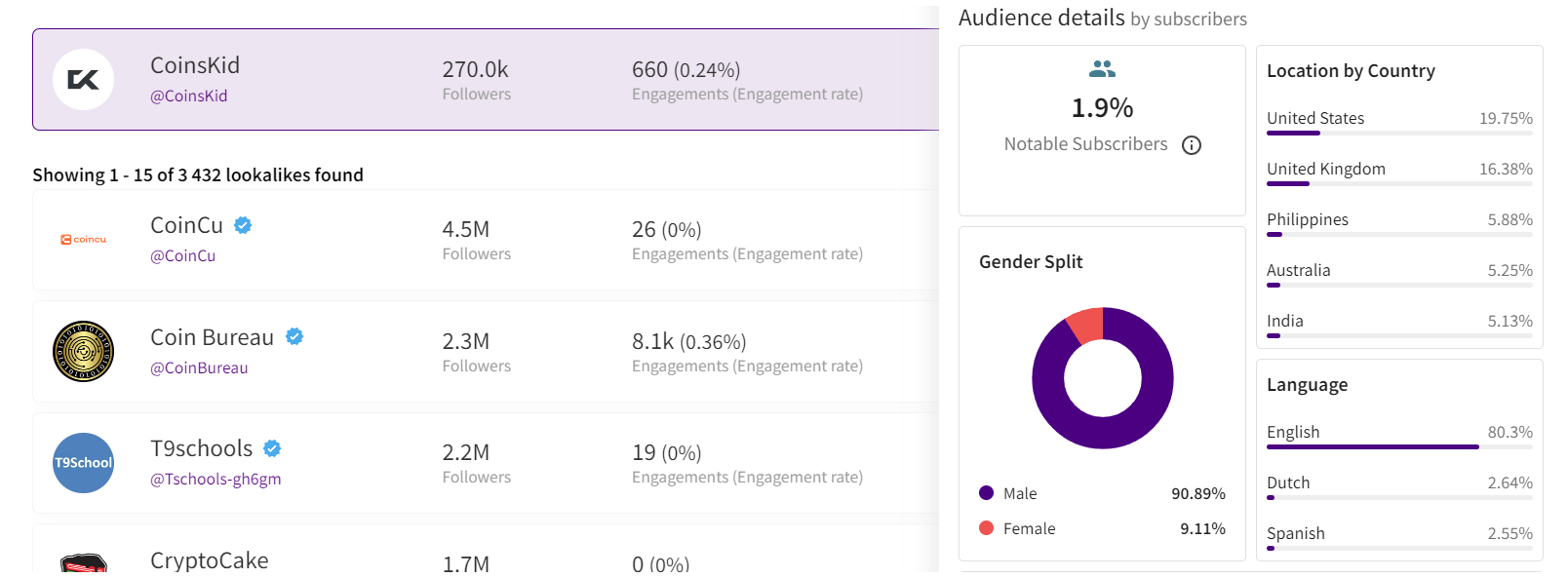

3. Influencer’s channel statistics

The primary statistics of interest are region and demographic split, and sometimes the device types of the viewers.

LEVEL 1

When reviewing the shared statistics, the first step is to request a video screencast instead of a simple screenshot. This is because it takes more time to organically edit a video than a screenshot, making it harder to manipulate the statistics. If the creator refuses, step two (if only screenshots are provided) is to download them and check the file’s properties on your computer. Look for details such as whether it was created with Adobe Photoshop or the color profile, typically Adobe RGB, to determine if the screenshot has been edited.

LEVEL 2

After confirming the authenticity of the stats screenshot, it’s crucial to analyze the data. For instance, if you’re examining a channel conducted in Spanish with all videos filmed in the same language, it would raise concerns to find a significant audience from countries like India or Turkey. This discrepancy, where the audience doesn’t align with regions known for speaking the language, is a red flag.

If we’re considering an English-language crypto channel, it typically suggests an international audience, as English’s global use for quality educational content on niche topics like crypto. However, certain considerations apply. For instance, if an English-speaking channel shows a significant percentage of Polish viewers (15% to 30%) without any mention of the Polish language, it could indicate fake followers and views. However, if the channel’s creator is Polish, occasionally posts videos in Polish alongside English, and receives Polish comments, it’s important not to rush to conclusions.

Example of statistics

Example of statistics

Wrapping up

These are the main factors to consider when selecting an influencer to promote your crypto product. Once you’ve launched the campaign, there are also some markers to show which creators did bring the authentic traffic and which used some tools to create the illusion of an active and engaged audience. While this may seem obvious, it’s still worth mentioning. After the video is posted, allow 5-7 days for it to accumulate a basic number of views, then check performance metrics such as views, clicks, click-through rate (CTR), signups, and conversion rate (CR) from clicks to signups.

If you overlooked some red flags when selecting crypto channels for your launch, you might find the following outcomes: channels with high views numbers and high CTRs, demonstrating the real interest of the audience, yet with remarkably low conversion rates. In the worst-case scenario, you might witness thousands of clicks resulting in zero to just a few signups. While this might suggest technical issues in other industries, in crypto campaigns it indicates that the creator engaged in the campaign not only bought fake views and comments but also link clicks. And this happens more often than you may realize.

Summing up, choosing the right crypto creator to promote your product is indeed a tricky job that requires a lot of resources to be put into the search process.

Author

Nadia Bubennikova, Head of agency at Famesters

The BIS, along with seven leading central banks and a cohort of private financial firms, has embarked on an ambitious venture known as Project Agorá.

Named after the Greek word for “marketplace,” this initiative stands at the forefront of exploring the potential of tokenisation to significantly enhance the operational efficiency of the monetary system worldwide.

Central to this pioneering project are the Bank of France (on behalf of the Eurosystem), the Bank of Japan, the Bank of Korea, the Bank of Mexico, the Swiss National Bank, the Bank of England, and the Federal Reserve Bank of New York. These institutions have joined forces under the banner of Project Agorá, in partnership with an extensive assembly of private financial entities convened by the Institute of International Finance (IIF).

At the heart of Project Agorá is the pursuit of integrating tokenised commercial bank deposits with tokenised wholesale central bank money within a unified, public-private programmable financial platform. By harnessing the advanced capabilities of smart contracts and programmability, the project aspires to unlock new transactional possibilities that were previously infeasible or impractical, thereby fostering novel opportunities that could benefit businesses and consumers alike.

The collaborative effort seeks to address and surmount a variety of structural inefficiencies that currently plague cross-border payments. These challenges include disparate legal, regulatory, and technical standards; varying operating hours and time zones; and the heightened complexity associated with conducting financial integrity checks (such as anti-money laundering and customer verification procedures), which are often redundantly executed across multiple stages of a single transaction due to the involvement of several intermediaries.

As a beacon of experimental and exploratory projects, the BIS Innovation Hub is committed to delivering public goods to the global central banking community through initiatives like Project Agorá. In line with this mission, the BIS will soon issue a call for expressions of interest from private financial institutions eager to contribute to this ground-breaking project. The IIF will facilitate the involvement of private sector participants, extending an invitation to regulated financial institutions representing each of the seven aforementioned currencies to partake in this transformative endeavour.

Source: fintech.globa

The post Central banks and the FinTech sector unite to change global payments space appeared first on HIPTHER Alerts.

TD Bank has inked a multi-year deal with Google Cloud as it looks to streamline the development and deployment of new products and services.

The deal will see the Canadian banking group integrate the vendor’s cloud services into a wider portion of its technology solutions portfolio, a move which TD expects will enable it “to respond quickly to changing customer expectations by rolling out new features, updates, or entirely new financial products at an accelerated pace”.

This marks an expansion of the already established relationship between TD Bank and Google Cloud after the group previously adopted the vendor’s Google Kubernetes Engine (GKE) for TD Securities Automated Trading (TDSAT), the Chicago-based subsidiary of its investment banking unit, TD Securities.

TDSAT uses GKE for process automation and quantitative modelling across fixed income markets, resulting in the development of a “data-driven research platform” capable of processing large research workloads in trading.

Dan Bosman, SVP and CIO of TD Securities, claims the infrastructure has so far supported TDSAT with “compute-intensive quantitative analysis” while expanding the subsidiary’s “trading volumes and portfolio size”.

TD’s new partnership with Google Cloud will see the group attempt to replicate the same level of success across its entire portfolio.

Source: fintechfutures.com

The post TD Bank inks multi-year strategic partnership with Google Cloud appeared first on HIPTHER Alerts.

-

Latest News7 days ago

Trakx launches a new product: Trakx USDc Earn CTI powered by OpenTrade

-

Latest News6 days ago

Money20/20 Asia 2024: Days Two Roundup

-

Latest News3 days ago

Letter from Gatemore Capital Management LLP to Elementis PLC

-

Latest News6 days ago

Stripe Unveils Unbundled Payments Strategy in Fintech Pivot

-

Latest News3 days ago

Shanghai Electric Releases ESG Report, Highlighting Sustainable Development Achievements in 2023

-

Latest News7 days ago

Sungrow Released Annual Report 2023: Operating Revenue Witnessed A Robust Growth of 79.5%

-

Latest News6 days ago

Chubb Report: Damage During Home Renovations and from Extreme Weather are Top Concerns of U.K. High Earners

-

Latest News5 days ago

Former Tesla executive Tim Newell is set to spin off Aspiration’s consumer financial services division.